Introduction:

Using your emergency fund feels uncomfortable for most people. Even when the situation clearly called for it — a medical bill, a job loss, a car breakdown — there’s often this lingering anxiety afterward. The cushion is gone. Or at least thinner than it was.

That feeling is actually useful. It means you understand what that money was doing for you. Now the job is to rebuild your emergency fund and get that security back.

This article walks you through exactly how to do that — practically, without overwhelming yourself, and in a way that actually sticks.

First, Give Yourself a Moment Before Jumping Into Rebuild Mode

Here’s something most financial articles skip: before you start aggressively trying to rebuild your emergency fund, make sure the emergency is actually over.

This sounds obvious. But it’s easy to start redirecting money into savings while you’re still dealing with the situation that caused the withdrawal. If you just lost your job, for example, your first priority is stabilizing your monthly expenses — not rebuilding savings.

Wait until your situation is genuinely stable. Then turn your attention to replenishing what was used.

Trying to save while you’re still in crisis mode often just leads to withdrawing the money again a few weeks later. That cycle is discouraging and counterproductive.

Assess Exactly How Much You Used

Before you can rebuild your emergency fund, you need to know the actual number you’re working with.

This seems basic, but a lot of people are vague about it. “I used some of my savings” doesn’t give you a target. “I used $2,400 and my fund is now at $800 instead of $3,200” gives you something to work with.

Pull up your account and write down two things:

- What your emergency fund balance is right now

- What your target balance should be (typically 3–6 months of essential expenses)

The gap between those two numbers is your rebuilding goal. Having a specific number in front of you makes the process feel more manageable and measurable.

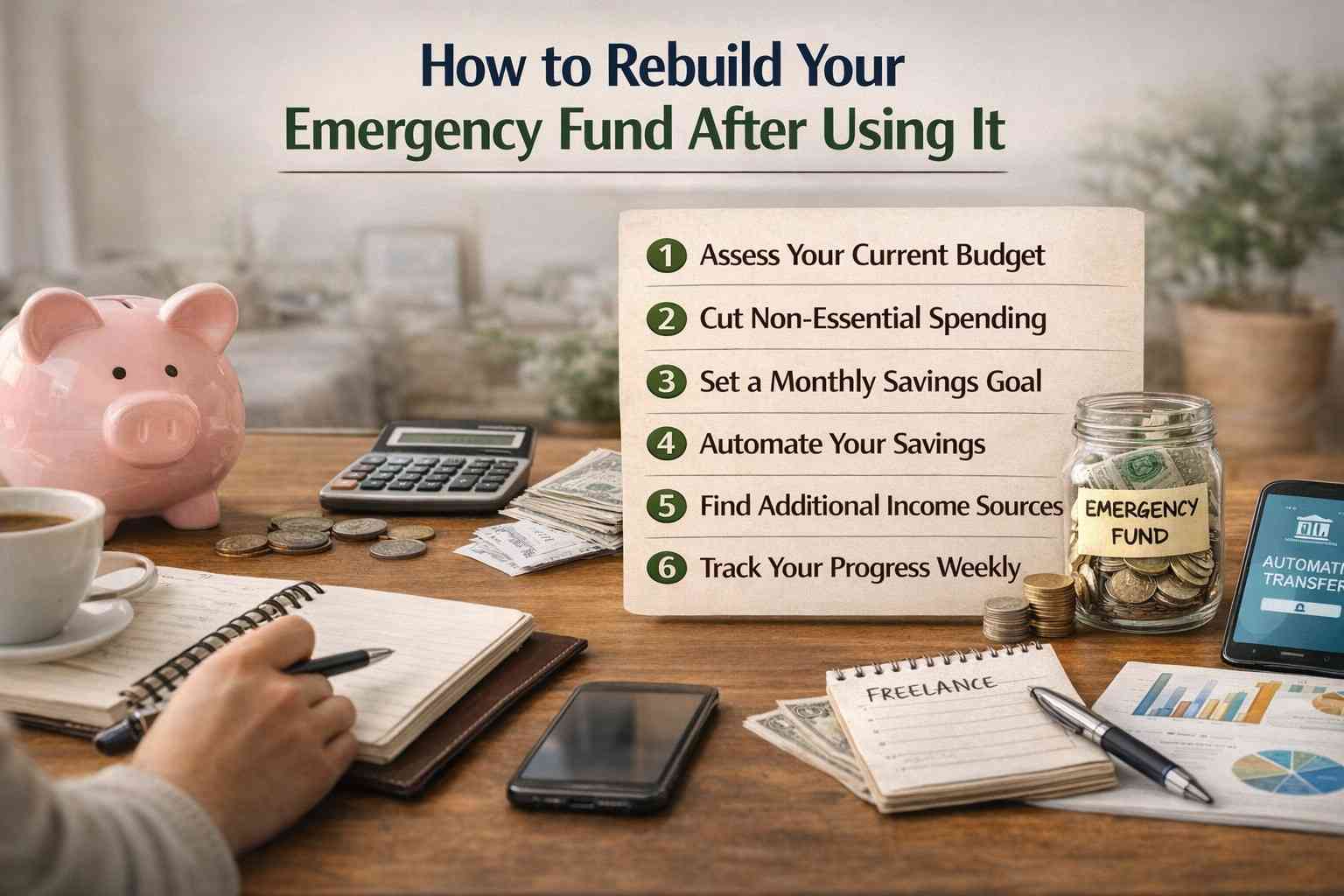

Rebuild Your Emergency Fund in Phases, Not All at Once

One of the biggest mistakes people make when trying to rebuild is setting a goal that’s too aggressive too fast. They feel behind, so they try to catch up quickly — and then burn out or fall short and lose motivation.

A phased approach works better.

Phase 1: Get Back to One Month’s Expenses

Your first goal when you rebuild your emergency fund isn’t to fully replace everything. It’s just to get back to having one month of essential expenses covered.

That’s rent or mortgage, basic groceries, utilities, minimum debt payments, and transportation. Just the necessities.

This first phase typically feels achievable within a few weeks to a couple of months depending on your income. Reaching it gives you a real confidence boost.

Phase 2: Return to Your Previous Balance

Once you’ve hit one month, the next milestone is simply getting back to what you had before the emergency hit.

This is your original fund restored. Psychologically, reaching this point feels like getting back to baseline — you’re not behind anymore.

Phase 3: Reassess and Possibly Grow Beyond the Original Amount

After you’ve rebuilt your emergency fund to where it was, pause and ask: was that amount actually enough? Did the emergency reveal that you needed more cushion than you thought?

If the emergency wiped out most of your fund, maybe the original target was a bit low for your situation. This is a good time to reconsider whether three months of expenses is the right target, or whether six months would give you more genuine security.

Create a Dedicated Monthly Transfer

The most reliable way to rebuild your emergency fund isn’t willpower. It’s automation.

Set up a recurring transfer from your checking account to your emergency savings — ideally scheduled for the same day you get paid. Even if it’s a small amount, say $50 or $100 per paycheck, the consistency is what matters.

You don’t notice money you never see sitting in your checking account. Automating the transfer removes the decision from the equation entirely.

Most banks and credit unions let you set up scheduled transfers through their app or website. It takes about five minutes and then you don’t have to think about it again.

If your income is irregular — freelance work, contract jobs, gig work — the automation piece is trickier. In that case, try the percentage method: whenever money comes in, move a fixed percentage directly to savings before spending anything. Even 5–10% adds up over time.

Temporarily Trim Discretionary Spending

This isn’t about extreme deprivation. Nobody is suggesting you live on rice and skip all enjoyment for six months just to rebuild your emergency fund faster.

But there are usually a few spending categories that, if you look honestly, could be trimmed for a while without seriously affecting your quality of life.

Streaming subscriptions you barely use. Takeout frequency. Impulse purchases. Subscription boxes. Small daily purchases that quietly drain $30–50 a month without much return.

Redirecting even $75–150 a month from these categories into your savings can meaningfully speed up the rebuilding process. And because it’s temporary — with a defined end point — it doesn’t feel like permanent sacrifice.

The key is being honest with yourself. Most people know where the money goes if they actually look at their bank statement.

Use Windfalls Strategically

Any unexpected money that comes your way while you’re trying to rebuild your emergency fund is an opportunity.

A tax refund. A work bonus. A gift. Selling something you no longer use. A freelance project that paid more than expected.

You don’t have to put 100% of every windfall into savings. That can feel punishing. But directing 50–70% of any unexpected money toward your fund significantly accelerates the timeline.

The other 30–50% can go toward something you want or need. This balance keeps the process sustainable because you still feel like you’re getting something, not just endlessly saving.

Avoid Adding New Debt While Rebuilding

This one is important. If you’re trying to rebuild your emergency fund while simultaneously accumulating new credit card debt, you’re often running in place.

The interest on credit card debt typically outpaces what you’re earning in a savings account. So the math isn’t in your favor.

This doesn’t mean you can’t use a credit card at all. It means being careful not to let balances grow while you’re in rebuild mode. Pay off what you charge each month if possible.

If you already have existing debt, the decision of whether to prioritize debt payoff or savings rebuild isn’t always straightforward. A general rule that works for many people: build a small starter emergency fund first (around $500–$1,000), then aggressively pay down high-interest debt, then return to fully rebuilding the emergency fund. This sequence gives you a buffer while also attacking expensive debt.

Keep the Rebuilt Fund in the Right Place

While you’re rebuilding, make sure the account you’re saving into is actually working for you. This is easy to overlook when you’re focused on the savings habit itself.

A high-yield savings account will earn meaningfully more interest than a standard savings account at a traditional bank. In 2026, the difference in APY between the two can be significant enough to actually matter, especially as your balance grows.

Keeping your rebuilt emergency fund in a separate account — not your checking account, not a joint spending account — also helps prevent accidental spending. Out of sight really does mean out of mind for most people.

If you want to explore which account types are best suited for emergency savings, understanding the difference between high-yield savings accounts and money market accounts can help you make a more informed decision.

Track Your Progress Visibly

This sounds minor but genuinely makes a difference. When you can see your progress, you stay motivated.

Some people use a simple spreadsheet. Others use a savings tracker app. Some even draw a paper thermometer on a sticky note and color it in as the balance grows. Whatever format you’ll actually look at.

Checking in on your rebuild progress once a week — even briefly — keeps it in your awareness and helps you notice if you’ve fallen off track before too much time passes.

You’re essentially training yourself to treat “rebuild the emergency fund” as an active, ongoing goal rather than a vague intention.

What to Do If a Second Emergency Hits While You’re Rebuilding

Life doesn’t pause while you’re trying to rebuild your emergency fund. Sometimes another unexpected expense shows up before you’ve finished replenishing.

First — don’t panic. This is what the partial fund is there for. Even a partially rebuilt emergency fund is better than nothing.

Second — if the new situation is genuinely urgent and necessary, use what you have. That’s the whole point. Then restart the rebuild from wherever you land.

Third — if the new situation is not truly an emergency (and it’s worth being honest about this), find another way to handle it. A payment plan. Temporarily reducing another expense. Looking at whether a non-essential purchase can be delayed.

Understanding what actually qualifies as a true financial emergency before you withdraw again helps you protect the fund during its vulnerable rebuilding period.

How Long Does It Usually Take to Rebuild?

Honestly? It depends on a few things: how much you used, what your income looks like, and how consistently you save.

For someone who drained half their fund and has a moderate income with room to save $200–300 a month, getting back to the original balance typically takes four to twelve months.

For someone who used their entire fund and is working with a tighter budget, it might take longer — potentially a full year or more.

Neither timeline is a failure. The only thing that matters is that you’re moving in the right direction consistently. Slow progress is still progress.

Final Conclusion: Rebuild Your Emergency Fund

Using your emergency fund was the right call if the situation called for it. Now the focus shifts: rebuild your emergency fund steadily, methodically, and without burning yourself out in the process.

The phased approach — one month, then your original balance, then a reassessment — keeps the goal from feeling overwhelming. Automating your transfers removes the daily decision. Being honest about discretionary spending and using windfalls wisely speeds things up. And tracking progress keeps you motivated when the finish line feels far away.

You built the fund once. You can rebuild your emergency fund again — often smarter and stronger than before.