Introduction: What Counts as a True Financial Emergency

Most people have been there. Something unexpected happens, the stomach drops, and the brain immediately jumps to: “This is an emergency. I need to use my savings.”

Sometimes that’s absolutely the right call. Other times, it really isn’t — but the stress of the moment makes it hard to think clearly.

Understanding what counts as a true financial emergency is one of those things nobody really teaches you. It sounds obvious until you’re standing at the pharmacy counter, or your car makes a noise it’s never made before, or your phone screen cracks into seventeen pieces. Suddenly the line between “emergency” and “inconvenience” gets very blurry.

This article is going to clear that up. Practically. Honestly. Without sugarcoating.

Why This Distinction Matters More Than You Think

Your emergency fund exists for one reason: to protect you when life genuinely goes sideways. Not when life gets mildly annoying. Not when there’s a sale on something you’ve been wanting. When things actually go wrong.

If you dip into that fund for non-emergencies, you’ll find yourself with an empty safety net exactly when you need it most. That’s the real danger.

Knowing what counts as a true financial emergency isn’t about being strict with yourself for no reason. It’s about making sure the money is there when the real thing hits.

And real emergencies do happen. More often than we plan for.

The Core Test: Three Questions to Ask Yourself

Before we get into specific examples, here’s a simple three-part test. When something unexpected comes up, ask:

1. Is this urgent? Does it need to be handled within days, not weeks?

2. Is it necessary? Would ignoring it cause serious harm — to your health, housing, income, or safety?

3. Was it truly unplanned? Is this something you couldn’t have reasonably anticipated and saved for in advance?

If all three answers are yes, you’re probably looking at a genuine financial emergency. If even one answer is no, pause before touching your savings.

This three-question filter is simple but surprisingly effective. Most “emergencies” that aren’t actually emergencies fail at question two or three.

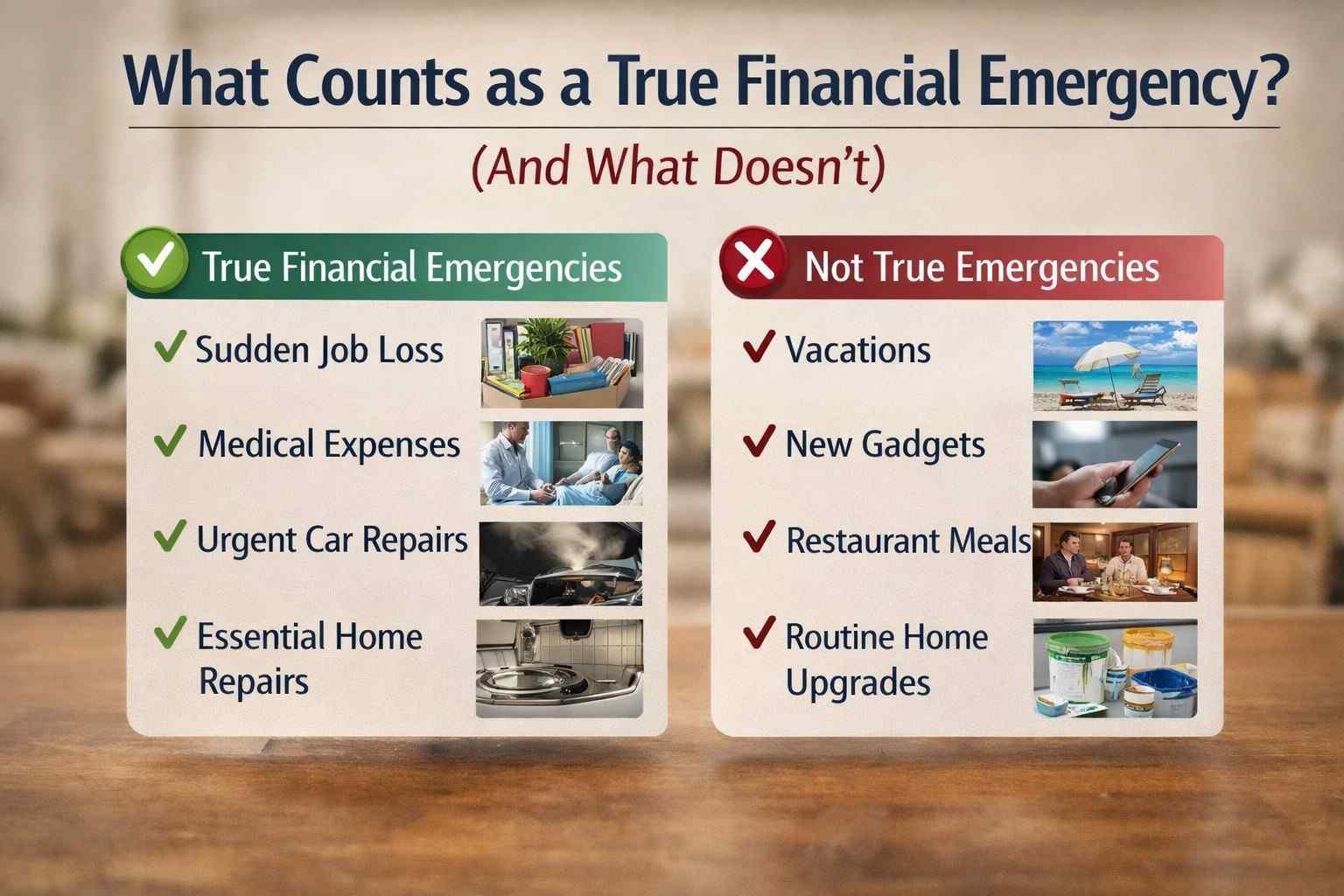

What Counts as a True Financial Emergency

Let’s go through the real ones. The situations where using your emergency fund is not only acceptable — it’s the right decision.

Sudden Job Loss

Losing your income without warning is one of the clearest examples of what counts as a true financial emergency. Rent still comes due. Groceries still need buying. Bills don’t pause because your employer let you go.

Your emergency fund is literally designed for this. Use it to cover essentials while you search for new work — not to maintain your full lifestyle, but to handle the basics.

Unexpected Medical or Dental Expenses

A sudden illness, an accident, an emergency dental situation — these aren’t predictable, and they often come with costs that can’t be delayed.

If you need medication you can’t skip, a procedure that can’t wait, or urgent care that your insurance doesn’t fully cover, that qualifies. This is exactly what counts as a true financial emergency in the medical sense.

Note: routine checkups and planned procedures don’t qualify. Those can be saved for separately.

Essential Car Repairs

Not every car problem counts. But if your car breaks down and you need it to get to work — and there’s no realistic public transit alternative — fixing it becomes urgent and necessary.

Brakes failing. Engine issues that make the car unsafe or undriveable. A transmission problem that leaves you stranded. These are legitimate.

A scratched bumper or a minor cosmetic dent? That’s not what counts as a true financial emergency. That can wait.

Critical Home Repairs

Your roof develops a serious leak in the middle of rainy season. Your heating system fails in winter. A pipe bursts and water is actively damaging your home.

These are situations where delaying repair causes greater harm or cost. That makes them emergencies.

A chipped tile in the bathroom or a broken cabinet hinge? Annoying, yes. An emergency requiring immediate savings withdrawal? No.

Losing Housing Unexpectedly

Being suddenly displaced — through an eviction notice you weren’t prepared for, a landlord selling the property, or a domestic situation requiring you to leave quickly — is a genuine crisis that justifies emergency fund use.

Finding temporary housing, covering a deposit, or managing moving costs in a tight timeline is exactly the kind of situation this money is meant for.

What Does NOT Count as a True Financial Emergency

This is where it gets uncomfortable. Because some of the things people regularly use their emergency savings for are not actually emergencies. They’re just expenses that felt urgent in the moment.

Sales, Deals, and “Limited Time” Offers

A flash sale on a laptop you’ve been eyeing. A travel deal that disappears in 48 hours. A discount on a phone upgrade that feels too good to pass up.

None of these are emergencies. The urgency is manufactured by the seller, not by your actual life circumstances. This is not what counts as a true financial emergency — it’s marketing working exactly as intended.

Planned Events You Forgot to Save For

A friend’s wedding you knew about for eight months. A birthday party. A holiday trip that happens every single year at the same time.

These are absolutely things you should budget and save for. But because they’re predictable, they don’t qualify as unexpected emergencies. If you didn’t save in time, that’s a budgeting problem — not an emergency fund situation.

Routine Car Maintenance

Oil changes, tire rotations, replacing worn brake pads on a schedule — these are predictable costs of owning a vehicle. They should come from your regular budget, not your emergency savings.

If you’re regularly pulling from your emergency fund for maintenance, it might be worth setting up a separate small “car fund” you contribute to monthly.

Subscription Renewals and Annual Fees

Your Amazon Prime auto-renewed. Your phone plan jumped in price. Your annual software subscription hit your account.

Again — predictable. These can be planned for. They’re not emergencies, even if they caught you off guard this particular month.

Wanting a Newer Version of Something That Still Works

Your current Android phone works fine. It’s maybe two years old. But the new model just dropped and it looks incredible.

This is not what counts as a true financial emergency. Wants and emergencies are fundamentally different categories, even when the want feels very strong.

The Gray Area: Things That Feel Like Emergencies But Need More Thought

Some situations genuinely sit in the middle. These aren’t clear-cut, and they deserve honest reflection.

Pet Emergencies

Vet bills for a sick or injured pet can be significant and truly unexpected. If your pet needs urgent care and you have no pet insurance, this does feel like an emergency — and for many people, it emotionally is one.

Whether it qualifies as a financial emergency depends on the situation. A necessary surgery to save your pet’s life hits different than optional cosmetic procedures. Use judgment here.

Helping Family Members

A parent who needs help with rent. A sibling facing eviction. These situations tug hard.

But here’s the honest reality: regularly supporting others from your emergency fund can leave you vulnerable. It’s worth asking whether this is truly a one-time crisis or a recurring situation that needs a different kind of solution.

Helping someone else is kind. Depleting your safety net repeatedly is risky for everyone involved.

Job-Related Expenses for a New Role

Got a job offer that requires a professional certification, specific tools, or work clothes you don’t own? There’s an argument this is urgent and necessary — it directly protects your income.

This is borderline. If it’s a small amount you can cover from your regular budget, do that first. If it’s substantial and the opportunity is genuinely time-sensitive, it might qualify.

How to Build Better Habits Around Emergency Fund Use

Understanding what counts as a true financial emergency is the first step. Building habits that protect your fund is the next one.

Create Separate Sinking Funds

A sinking fund is just a small savings bucket for a predictable expense. Car maintenance fund. Annual subscription fund. Holiday gift fund. Pet care fund.

When these categories have their own small reserves, you stop raiding your emergency savings for things that were always going to happen.

Write Down Your Personal Emergency Criteria

Seriously — take five minutes and write out what you consider a genuine emergency. Make it specific. When the stressful moment arrives, you’ll have a reference point that isn’t clouded by panic.

Give Yourself a 48-Hour Rule for Non-Obvious Situations

If you’re not sure whether something counts as a real emergency, wait 48 hours before withdrawing anything. In genuine emergencies, waiting a day or two usually doesn’t change the outcome much. In non-emergencies, the urgency often fades.

Teaching This to Others in Your Household

If you share finances with a partner, family member, or roommate, having a shared understanding of what counts as a true financial emergency is genuinely important.

Disagreements about this are more common than you’d think. One person sees a broken laptop as an emergency (it’s needed for work). The other sees it as an upgrade opportunity. Neither is necessarily wrong — but without a shared framework, these disagreements can cause real tension.

Have the conversation before an emergency happens. It’s much easier to agree on criteria when there’s no stress involved.

Final Conclusion: What Counts as a True Financial Emergency

The line between a real financial emergency and an uncomfortable expense isn’t always perfectly clear. But it’s clearer than most people give it credit for.

What counts as a true financial emergency generally comes down to three things: it’s urgent, it’s necessary, and it was genuinely unplanned. Job loss, sudden medical needs, critical home or car repairs, unexpected housing crises — these are the real ones. Sales, planned events you forgot to save for, and lifestyle upgrades are not, even when they feel pressing.

Your emergency fund is one of the most valuable financial tools you have. Protecting it means protecting yourself. The better you understand when to use it — and when not to — the more secure your financial foundation becomes over time.