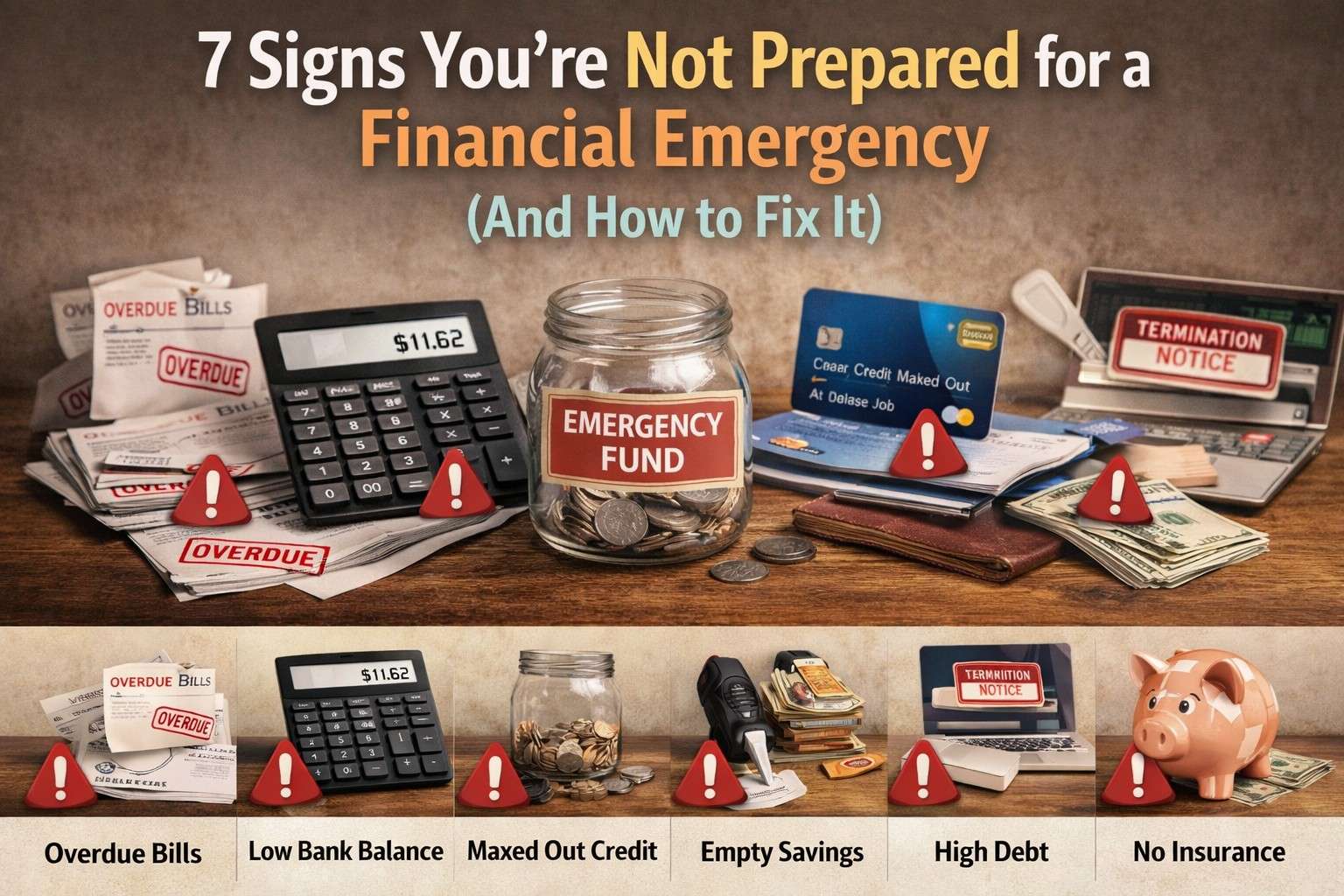

Introduction: Not Prepared for a Financial Emergency

Most people assume they’re reasonably prepared for the unexpected. Until they’re not.

A sudden job loss, an urgent car repair, an unexpected medical bill — these things have a way of arriving without warning and exposing exactly how thin the financial safety net really is. The uncomfortable truth is that a large number of people are not prepared for a financial emergency, even those who would describe themselves as “pretty good with money.”

The tricky part is that the signs aren’t always obvious. Nobody wakes up and thinks, “I am dangerously unprepared.” It creeps up quietly — through small habits, ignored warnings, and deferred decisions.

This article walks through seven clear signs that your financial cushion isn’t where it needs to be, and more importantly, what you can actually do about each one.

Sign 1: You Have Less Than One Month of Expenses Saved

This is the most direct indicator that you’re not prepared for a financial emergency. If your savings account balance couldn’t cover your rent, groceries, utilities, and transportation for even thirty days — that’s a real vulnerability.

Most financial guidance recommends three to six months of essential expenses as a minimum target. But even reaching one month is a meaningful starting point that many people haven’t hit.

The fix here isn’t complicated, even if it takes time. Start with a small, specific target: $500. Then $1,000. Then one full month. Break it into steps rather than staring at the whole mountain.

Set up an automatic transfer — even $25 or $50 per paycheck — into a separate savings account. Consistency matters far more than the amount when you’re starting from scratch.

Sign 2: Your Emergency Fund Is Mixed With Your Regular Spending Money

Some people technically have savings, but it’s all sitting in the same checking account they use for daily purchases. That’s not really an emergency fund — that’s just money that hasn’t been spent yet.

When emergency savings and spending money share an account, the psychological separation disappears. You see a higher balance and you spend more. Or the money quietly gets chipped away by small purchases until there’s nothing left when something real happens.

Being not prepared for a financial emergency sometimes looks exactly like this: money exists, but it’s not protected.

The fix is simple. Open a separate savings account — preferably at a different bank or at least with a meaningful barrier between it and your everyday spending. A high-yield savings account works well here because it earns a decent return and the slight inconvenience of transferring funds out actually helps prevent casual dipping.

Out of sight, out of reach, out of mind. That separation is surprisingly powerful.

Sign 3: You Rely on Credit Cards as Your Backup Plan

“If something serious happens, I’ll just put it on the card.” This thought feels reasonable. It’s also a sign that you’re not prepared for a financial emergency in the truest sense.

Credit cards can bridge a gap in a genuine pinch. But they’re not an emergency fund. They come with interest rates that can range from 18% to well above 25%, and using them in a crisis often means spending months — sometimes years — paying off that original emergency with compounding interest added on top.

What starts as a $1,500 car repair can quietly become $2,100 by the time it’s fully paid off. The emergency is over, but the financial damage keeps going.

The fix isn’t to cut up all your credit cards. It’s to build actual liquid savings so that credit becomes a last resort rather than the plan. Start small, stay consistent, and treat saving as a non-negotiable monthly expense rather than whatever’s left over.

Sign 4: You Have No Idea What Your Monthly Essential Expenses Actually Are

This one surprises people. But being not prepared for a financial emergency often starts with not knowing your own numbers.

If someone asked you right now, “How much do you need each month to cover rent, food, utilities, and basic transport?” — could you answer within $200 of accuracy? Many people genuinely couldn’t.

Not knowing this number means you can’t calculate how much emergency fund you actually need. You end up with a vague, unmeasurable goal like “save more money,” which is easy to perpetually postpone.

The fix is a one-time exercise: sit down for 30–45 minutes and go through the last two or three months of bank statements. Add up only the essentials — not subscriptions, not dining out, not entertainment. Just the non-negotiables.

That number becomes your monthly baseline. Multiply it by three for your minimum emergency fund target. Now you have a real goal with a real number attached.

Sign 5: A Single Unexpected Expense Would Force You Into Debt

Here’s a practical test: if your phone screen cracked tomorrow and the repair cost $180, how would you handle it? What about a $600 car repair? A $1,200 medical bill?

If the honest answer to any of those is “I’d have to put it on credit” or “I’d need to borrow from someone” — that’s a clear sign you’re not prepared for a financial emergency.

This isn’t about judgment. A lot of people are in exactly this position, and it usually happened gradually rather than through any single bad decision. But it does mean the safety net needs attention.

The fix involves two parallel steps. First, stop accumulating new debt where possible — even small, avoidable credit card balances. Second, start building a buffer specifically for these mid-size unexpected expenses, separate from your larger emergency fund. Some people call this a “small emergencies fund” — $300 to $500 just for the minor unexpected things that don’t qualify as true crises but still knock you off balance.

Sign 6: Your Income Is Irregular and You Have No Financial Buffer at All

Freelancers, gig workers, self-employed people, and anyone with variable income are in a particularly vulnerable position when they’re not prepared for a financial emergency.

When income is unpredictable, a slow month isn’t just inconvenient — it can be destabilizing. A month where work dries up unexpectedly becomes a genuine financial crisis if there’s nothing set aside.

People with stable salaries can sometimes get by with a thinner cushion because their income is reliable. For variable income earners, a larger emergency fund isn’t optional — it’s essential. Six to nine months of expenses is a more realistic target for someone whose income fluctuates significantly.

The fix for variable income earners involves a slightly different approach. Rather than saving a fixed monthly amount, save by percentage. When a strong month comes in, move 15–20% directly to savings before spending anything. In slower months, save what you can but don’t stress about the lower amount.

Building an income smoothing habit — essentially paying yourself a consistent “salary” from your variable income — also helps enormously. NerdWallet’s guide on managing irregular income covers this approach in practical detail.

Sign 7: You’ve Thought About Starting an Emergency Fund for Over a Year Without Acting

This last sign is the most honest one. And it’s the most common.

The information isn’t the problem. Most people reading this already know they should have an emergency fund. They’ve known for a while. The gap is between knowing and actually doing.

If you’ve been meaning to start, planning to start, almost starting — but haven’t moved any actual money anywhere yet — then you are, in practical terms, not prepared for a financial emergency. Intentions don’t pay bills during a crisis.

The fix for chronic delay isn’t more information. It’s reducing friction.

Open the savings account today, not this week. Not when things calm down. Today, during whatever window of time you have. Transfer even $10 to start. The point is to break the inertia.

Most people who finally act on this say the hardest part was just getting started. Once the account exists and has something in it, continuing becomes much easier. The first step is disproportionately difficult because it requires changing a pattern. Everything after that is just maintenance.

Why Being Not Prepared for a Financial Emergency Is More Common Than People Admit

There’s a social dimension to this that’s worth acknowledging. Financial unpreparedness is vastly more widespread than the conversation around it suggests.

People generally don’t advertise the fact that they’re living without savings. So everyone assumes their neighbors, colleagues, and friends are better prepared than they actually are. This creates a false sense of normalcy — “I’m doing about as well as everyone else, so I must be fine.”

The reality is that being not prepared for a financial emergency is the default position for a significant portion of adults across income levels. This isn’t a low-income problem or a young person problem. Plenty of high earners are equally underprepared because spending tends to rise with income if savings habits aren’t deliberately built.

Understanding this doesn’t lower the urgency of fixing it. But it does remove the shame spiral that sometimes stops people from taking action. You’re not uniquely irresponsible. You’re in a common situation that is completely fixable with deliberate steps.

Building Preparedness: A Practical Starting Point

If you recognized yourself in several of the signs above, here’s a practical sequence to start with:

Week one: Calculate your actual monthly essential expenses. Write down the number. This is your baseline.

Week two: Open a dedicated savings account if you don’t have one already. Make it separate from your daily spending account.

Week three: Set up an automatic recurring transfer — whatever you can commit to without fail. Even $30 a paycheck.

Month two and beyond: Revisit your discretionary spending and identify one or two areas you can redirect toward savings temporarily.

Understanding what genuinely counts as a financial emergency versus a regular expense also helps you protect the fund once it exists.

The goal isn’t perfection. It’s consistent forward movement. Every dollar added to your emergency fund is one step further from being not prepared for a financial emergency when life decides to test you.

Final Conclusion: Not Prepared for a Financial Emergency

The seven signs covered in this article aren’t meant to be alarming. They’re meant to be honest.

Being not prepared for a financial emergency isn’t a character flaw — it’s a fixable gap. But it does require actually fixing it, not just acknowledging it. Knowing the signs is only useful if it leads to changed behavior.

Whether you recognized one sign or all seven, the path forward is the same: start small, stay consistent, keep the money separate, and know your numbers. None of this requires a high income or financial expertise. It requires intention and follow-through.

The unexpected will arrive eventually. The only real variable is whether you’ll be ready when it does.