Introduction: Weekly Budget vs. Monthly Budget

There’s a question that comes up constantly in personal finance conversations — and it sounds deceptively simple. Should you budget weekly or monthly?

Most people default to monthly budgeting without ever questioning it. Salary comes once a month, rent is due once a month, bills are monthly — so budgeting monthly just feels logical. But a growing number of people are discovering that a weekly budget vs. monthly budget approach actually works better for how their brain processes spending decisions.

Neither system is universally superior. But one of them is almost certainly better suited to your specific income pattern, spending habits, and lifestyle. This article breaks down both approaches honestly — how each works, where each struggles, and how to figure out which one will actually save you more money in your real life.

Why the Budgeting Timeframe Matters More Than People Realize

Most budgeting advice focuses on what to track — categories, amounts, savings percentages. Very little attention goes to when you track. But the timeframe of your budget has a surprisingly large effect on how well it works.

A budget period that’s too long creates a false sense of abundance at the start of the period and panic at the end. Most people have experienced this with monthly budgeting — the first two weeks feel fine, and then suddenly the last week feels impossibly tight.

A budget period that’s too short creates friction and overhead — too many planning sessions, too much time spent managing small amounts.

The weekly budget vs. monthly budget decision is really a question about which timeframe matches how you naturally experience money. Get that right, and budgeting becomes significantly easier to maintain.

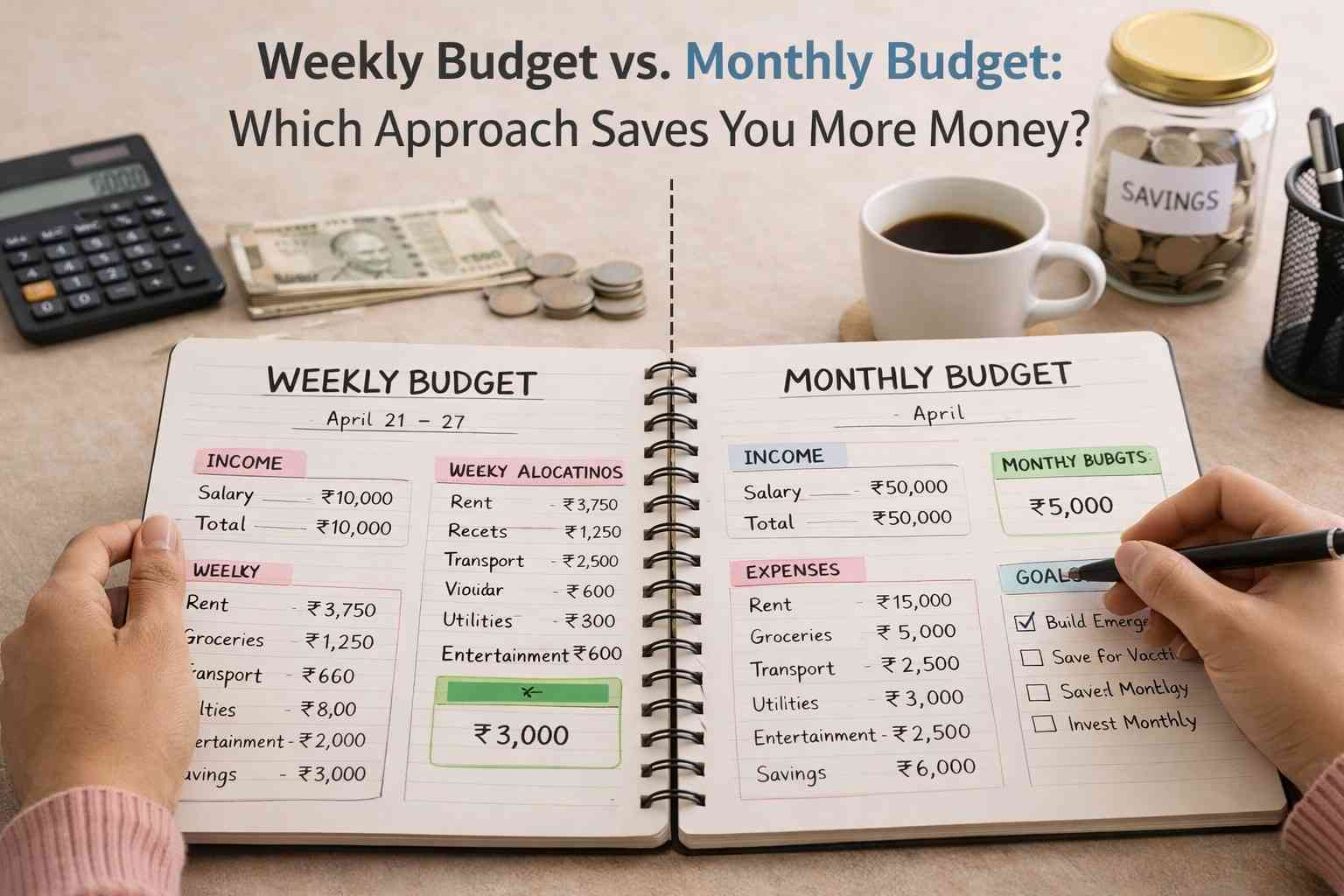

How Monthly Budgeting Works

Monthly budgeting is the standard approach. You sit down at the start of the month, look at your expected income, assign amounts to each spending category, and work within those limits for the next 30 or 31 days.

Most financial systems are designed around monthly cycles — salaries, rent, loan EMIs, insurance premiums, utility bills. So monthly budgeting has a natural alignment with how the financial world operates.

The typical monthly budget covers fixed expenses first — rent, EMIs, insurance. Then variable expenses like food, transport, and utilities. Then discretionary spending like entertainment and dining out. Finally, savings and investments get whatever is left — or ideally, whatever was set aside at the start.

For a detailed walkthrough of building this kind of plan properly, this guide on how to create a monthly budget plan in 5 simple steps covers the full process from income calculation to category setup.

The Real Strengths of Monthly Budgeting

Monthly budgeting aligns naturally with salary cycles. For someone paid once a month, there’s a clean logic to planning once a month. One income event, one planning session, one set of category limits for the period.

It also requires less frequent active management. You plan once, do weekly check-ins, and adjust if something goes off track. The administrative overhead is lower than budgeting weekly.

For people with stable, predictable expenses — a salaried employee whose rent, bills, and loan payments don’t change much — monthly budgeting provides enough structure without demanding constant attention.

The Real Weaknesses of Monthly Budgeting

The 30-day view is actually quite long when it comes to spending psychology. Most people can’t clearly visualize ₹45,000 spread across 30 days. The number feels large at the start. By day 20, it’s gone and you’re not sure how.

Monthly budgets also tend to mask overspending until it’s too late to correct. If you’re checking in weekly, you might notice on day 10 that your food budget is already 60% spent. If you only look at the monthly picture, you might not register that as a problem until the month is over.

The weekly budget vs. monthly budget problem shows up most clearly here — the longer the window, the more opportunities for small daily overspending to accumulate invisibly.

How Weekly Budgeting Works

Weekly budgeting divides your monthly income into weekly spending allowances. Instead of thinking “I have ₹45,000 this month,” you think “I have roughly ₹10,500 this week.”

There are two main approaches to setting this up. The first is dividing monthly income by four — simple, consistent, easy to calculate. The second is slightly more sophisticated: you identify which expenses hit in which week of the month and plan each week individually based on that.

The second approach is more accurate but takes more setup time. For most beginners, dividing by four is a perfectly good starting point.

The Real Strengths of Weekly Budgeting

The most significant advantage in the weekly budget vs. monthly budget comparison is the shorter feedback loop. A week is a timeframe most people can visualize and manage intuitively. You can feel ₹10,000 for a week much more concretely than ₹40,000 for a month.

When you know you have ₹10,000 for the week and you’ve spent ₹7,500 by Thursday, the math is immediate and visceral. Three days left, ₹2,500 remaining. That clarity drives better daily decisions far more effectively than a distant monthly limit.

Weekly budgeting also creates natural reset points. A bad spending day on Tuesday doesn’t ruin the entire month — it just makes Wednesday through Sunday tighter. The psychological damage of one overspending event is contained to a single week rather than spreading guilt and anxiety across a full month.

This containment effect is one of the most underappreciated benefits in the weekly budget vs. monthly budget debate. Shorter periods mean smaller failures when things go wrong — and things always go wrong sometimes.

The Real Weaknesses of Weekly Budgeting

The obvious challenge is that not all expenses fit neatly into weekly boxes. Rent is monthly. Most insurance premiums are monthly or annual. Many bills arrive monthly. Dividing everything into weekly chunks requires either setting aside weekly amounts for monthly bills — which works but adds complexity — or handling large monthly expenses separately from the weekly spending plan.

Weekly budgeting also requires more frequent active engagement. You’re essentially doing four planning sessions a month instead of one. For someone already stretched for time, this can feel like too much overhead — and a budgeting system you don’t have time to maintain is a system that won’t last.

The Psychological Difference Between Weekly and Monthly

This is where the weekly budget vs. monthly budget comparison gets genuinely interesting — and where the answer for most people becomes clear.

Human brains are not naturally good at planning across 30-day periods. A month is abstract. A week is concrete. You know what a week feels like. You can picture Monday through Sunday and how money moves across those days.

Research in behavioral economics consistently shows that people make more careful spending decisions when the remaining budget period is shorter. When you have ₹10,000 for a week and it’s Thursday, the endpoint is close enough to feel real. When you have ₹45,000 for a month and it’s the 5th, the endpoint is so far away it barely registers.

This is why many people who struggle with monthly budgeting — who’ve tried it multiple times and watched it fall apart consistently — find that switching to weekly budgeting creates an almost immediate improvement. The timeframe change alone shifts the psychology enough to change the behavior.

Which Approach Saves More Money?

Here’s the direct answer: for most people, weekly budgeting saves more money — specifically for variable, day-to-day spending categories.

The reason is psychological proximity. Shorter time horizons create stronger spending awareness. When you’re managing weekly limits, every purchase gets evaluated against a number that feels immediate and real. Monthly limits feel too distant to create that same daily awareness.

However — and this matters — monthly budgeting is more practical for managing fixed expenses, large bills, and long-term savings goals. These items don’t fit naturally into weekly thinking.

The weekly budget vs. monthly budget question, when answered honestly, often leads to the same conclusion: the most effective system uses both. A monthly framework for fixed expenses and savings goals, and a weekly framework for variable day-to-day spending.

How to Use Both Systems Together

The hybrid approach is genuinely the most powerful answer to the weekly budget vs. monthly budget debate — and it’s simpler to set up than it sounds.

Step 1 — Handle Fixed Expenses Monthly

At the start of each month, set aside all your fixed, predictable expenses in one calculation. Rent, EMIs, insurance, fixed subscriptions — total these up and treat them as already spent. They’re not part of your weekly spending calculation.

Step 2 — Calculate Your Weekly Spending Money

Take what remains after fixed expenses and savings contributions. Divide by four. That’s your weekly variable budget — what’s available for food, transport, entertainment, personal care, and daily life.

For example: if take-home income is ₹48,000, fixed expenses total ₹22,000, and savings contribution is ₹6,000, then ₹20,000 remains for variable spending. Divided by four: ₹5,000 per week for daily life.

Step 3 — Track Weekly Spending Against the Weekly Number

This is where the behavioral benefit kicks in. Track your variable spending against ₹5,000 for the week — not ₹20,000 for the month. The smaller, more immediate number creates better daily awareness.

Check your remaining weekly balance every two or three days. On Android, a simple note in Google Keep or a quick update to a Sheets template takes less than two minutes.

Step 4 — Roll Over or Reset Each Week

Decide in advance what happens to unspent weekly money. Two common approaches: roll it over to the next week as a small bonus, or return it to savings at week’s end. Either works — what matters is that the decision is made in advance so there’s no temptation to treat leftover money as permission to splurge next week.

Weekly vs. Monthly: Who Should Use Which

After understanding both systems, the weekly budget vs. monthly budget choice becomes clearer based on a few personal factors.

Choose Monthly Budgeting If

Your income is stable and arrives once a month. Your expenses are largely predictable and don’t fluctuate much week to week. You find frequent planning sessions stressful or time-consuming. You have simple financial goals and a relatively consistent lifestyle.

Monthly budgeting with solid weekly check-ins covers most of what you need in this situation without demanding too much active management.

Choose Weekly Budgeting If

You’ve tried monthly budgeting multiple times and consistently run out of money before the month ends without understanding why. You have variable or irregular income that comes in weekly or irregularly. You tend to overspend in the first half of the month and scramble in the second half. You find daily spending decisions easier when you have a smaller, more immediate number to reference.

The weekly budget vs. monthly budget switch can create a noticeable improvement within the first two to three weeks for people who fit this profile.

Choose the Hybrid If

Your life has both stable fixed expenses and variable day-to-day spending that’s hard to control. You want the simplicity of monthly planning for big items and the behavioral benefit of weekly limits for everyday decisions. This is the approach most likely to produce the best long-term results for the widest range of people.

Common Mistakes With Both Systems

Whether you go weekly, monthly, or hybrid, a few predictable mistakes show up in the weekly budget vs. monthly budget comparison that are worth knowing in advance.

Forgetting irregular expenses in weekly planning — Vehicle servicing, medical costs, festival gifts — these don’t fit neatly into any single week or month. Both systems need a dedicated irregular expenses fund, funded a little each month regardless of which budgeting timeframe you use.

Treating the weekly reset as permission to start fresh with guilt-free spending — If you overspent last week, the new week isn’t a free pass. It’s a chance to be more careful, not to repeat the same pattern.

Using the monthly framework as an excuse to avoid weekly awareness — Monthly budgeting only works when paired with regular check-ins. A monthly plan reviewed once on the 1st and again on the 30th isn’t budgeting — it’s hoping.

For a broader look at how these timeframe decisions connect to overall budgeting philosophy, this breakdown of the best budgeting methods including zero-based and envelope approaches gives useful context on how weekly and monthly thinking fits into different budgeting frameworks.

Practical Tools for Each Approach on Android

Whichever side of the weekly budget vs. monthly budget debate you land on, your Android phone has everything you need to implement it.

For monthly budgeting: apps like Walnut or Money Manager track monthly category limits automatically. Google Sheets with a monthly template gives you full customization at zero cost.

For weekly budgeting: a simple weekly spending note in Google Keep — updated every time you spend — is fast and frictionless. A weekly tab in Google Sheets works well for people who prefer slightly more structure.

For the hybrid approach: maintain a monthly overview sheet for fixed expenses and savings, and a separate weekly tracking note or tab for variable spending. Two simple tools, used consistently, cover everything you need.

Final Conclusion: Weekly Budget vs. Monthly Budget

The weekly budget vs. monthly budget debate doesn’t have a single winner that works for every person in every situation. But it does have a clearer answer than most people expect.

Monthly budgeting provides the right framework for fixed expenses, savings goals, and big-picture financial planning. Weekly budgeting provides the psychological proximity that makes daily spending decisions more careful and more conscious. Together, they cover what neither does perfectly on its own.

If monthly budgeting has consistently failed you — if the money always runs out before the month does and you’re never quite sure why — try shifting your variable spending to a weekly framework. The change in how immediate and concrete your remaining budget feels can make a surprisingly large difference in how you actually spend day to day.

The goal isn’t to find the perfect system. It’s to find the system that keeps you paying attention to your money consistently, month after month. That consistency, more than any particular budgeting method or timeframe, is what actually builds financial stability over time.