Best Budgeting Methods of 2026: Envelope, Digital, and Zero-Based Explained

Introduction:

Nobody wakes up one morning and suddenly knows how to manage money well. It’s a skill — and like most skills, it gets a lot easier once you find the right approach for your specific situation.

That’s the real problem with most budgeting advice. It assumes one method works for everyone. In reality, the best budgeting methods for a salaried employee in a stable job look completely different from what works for a freelancer with unpredictable income, or a family managing multiple financial goals at once.

This guide breaks down three of the most effective and widely used best budgeting methods in 2026 — the envelope method, digital budgeting, and zero-based budgeting. Not in a textbook way. In a practical, honest way that helps you figure out which one actually fits your life.

Why Choosing the Right Budgeting Method Matters

Most people who try budgeting and quit don’t quit because they’re bad with money. They quit because they picked a method that didn’t match how they actually live.

Someone who hates tracking every transaction will fail with zero-based budgeting — not because zero-based is a bad system, but because it requires regular engagement that doesn’t fit their lifestyle. Someone who mostly uses UPI and cards for everything will struggle with a cash-only envelope system — not because envelopes don’t work, but because the method doesn’t match how they spend.

The best budgeting methods are the ones you’ll actually maintain. And the only way to find that is to understand what each method demands from you before you commit.

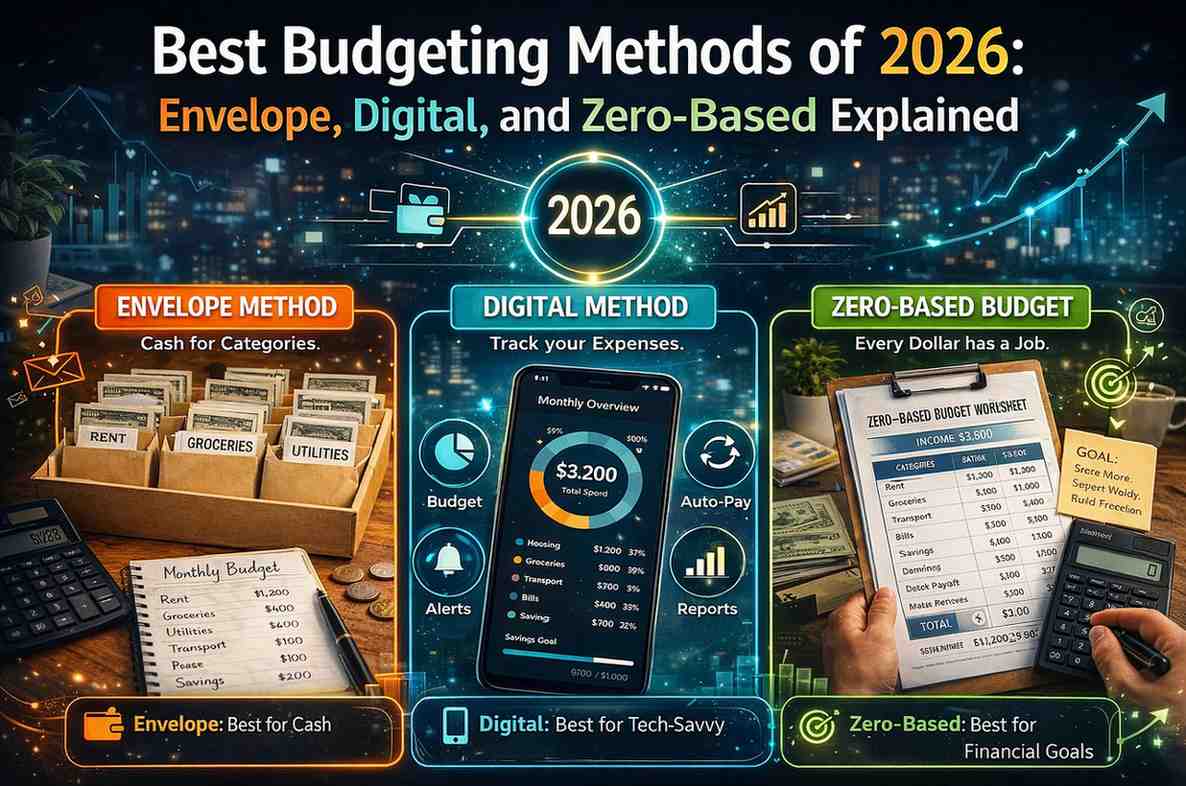

Method 1 — The Envelope Budgeting Method

The envelope method is one of the oldest personal finance tools around, and it’s still one of the best budgeting methods for people who overspend in specific categories and need something physical and tangible to create real spending limits.

The concept is simple. At the start of the month, you withdraw cash and divide it into labeled envelopes — one for groceries, one for transport, one for entertainment, and so on. Each envelope holds exactly the amount you’ve budgeted for that category. When the envelope is empty, spending in that category stops for the month.

No envelope shuffling. No borrowing from next month. The physical limitation is the entire point.

Why It Works

There’s solid psychological reasoning behind why the envelope method makes the list of best budgeting methods even in 2026. Paying with physical cash creates a very different mental experience than tapping a phone or swiping a card.

When you hand over actual notes, you feel the money leaving. That feeling creates friction — a small mental pause before spending — that digital payments completely bypass. Research in behavioral economics consistently shows that people spend more freely when paying digitally compared to paying with cash. The envelope method uses that psychology deliberately.

Who It Works Best For

The envelope method is particularly effective for people who consistently overspend in one or two specific categories — usually food, entertainment, or clothing. If you keep saying “I don’t know where my money goes” despite making decent income, the physical limitation of envelopes can break that pattern quickly.

It’s also genuinely useful for beginners who find digital budgeting apps overwhelming. There’s nothing to learn, no app to set up, no category to sync. You just put cash in envelopes and spend from them.

The Real Limitations in 2026

Let’s be honest about where the envelope method struggles. In India today, the majority of transactions happen via UPI, debit cards, and net banking. Withdrawing large amounts of cash each month feels impractical — and sometimes unsafe — for many people.

Rent, utility bills, online shopping, subscription services — none of these work with cash envelopes. So if you spend a significant portion of your income digitally, the envelope method alone won’t cover your whole financial picture.

The practical workaround is to use envelopes only for variable, cash-friendly categories — groceries, eating out, personal care, entertainment — while managing fixed and digital expenses separately. It’s a hybrid approach, and it works reasonably well.

Method 2 — Digital Budgeting

Digital budgeting is broadly one of the best budgeting methods for people who live most of their financial lives on their phones — which, in 2026, is most people.

Instead of cash and physical envelopes, digital budgeting uses apps, spreadsheets, or banking tools to track income and expenses automatically or semi-automatically. You set category limits, log or sync transactions, and check your spending dashboard to see where you stand at any point during the month.

Types of Digital Budgeting Tools

There are essentially three levels of digital budgeting, each requiring different amounts of effort.

Automated bank tracking — Some banks and UPI apps like Google Pay, PhonePe, or HDFC’s mobile banking automatically categorize your spending and show you a monthly breakdown. You don’t have to do anything manually. This is the lowest-effort version of digital budgeting and a good starting point for beginners.

Dedicated budgeting apps — Apps like Walnut, Money Manager, or YNAB (You Need A Budget) give you more control. You set your own category limits, log transactions (manually or via SMS sync), and get alerts when you’re approaching a category limit. These are among the best budgeting methods tools for people who want more detail without building everything from scratch.

Custom spreadsheets — Google Sheets on your Android phone gives you complete flexibility. You build the structure yourself, which takes more upfront time but lets you create something perfectly tailored to how your finances work. Many experienced budgeters prefer this because no app assumption gets in the way.

Why Digital Budgeting Fits 2026 Life

The obvious advantage is that digital budgeting matches how people actually transact today. If 90% of your spending happens via UPI and cards, a system built around tracking those transactions makes far more sense than withdrawing cash every month.

Digital budgeting also makes it easy to see patterns over time. After three months of tracking, you can see that your food spending spikes in December, your transport costs went down after you changed jobs, or your entertainment budget consistently runs out by the 20th. That kind of historical data is genuinely useful for making the best budgeting methods decision for your future months.

The Weakness of Digital Budgeting

The main limitation is psychological — the same one that makes cash envelopes powerful. Because digital spending feels frictionless, digital budgeting can become a tool for understanding overspending rather than preventing it.

You might track perfectly, know exactly how much you overspent on food, and still overspend the same amount next month. Awareness without behavioral friction doesn’t always change habits. Some people need the physical limitation of cash to actually modify their spending — not just observe it.

Method 3 — Zero-Based Budgeting

Zero-based budgeting consistently ranks among the best budgeting methods for people who are serious about taking full control of their finances — and it’s particularly powerful for those with specific financial goals, debt to pay off, or irregular income.

The core principle is that every rupee of your income gets assigned a specific job before the month begins. Income minus all allocations — including savings and investments — equals exactly zero. Not because you’ve spent everything, but because nothing is left unassigned.

For a complete step-by-step walkthrough of setting this up, this guide on how to build a zero-based budget from scratch covers the full process with a free template you can start using immediately.

How Zero-Based Budgeting Actually Works

You start with your total take-home income. Then you list every expense, saving goal, and investment — assigning a specific rupee amount to each. You keep adjusting until the total of all allocations exactly equals your income.

Every category gets a number. Groceries: ₹6,000. Emergency fund: ₹3,000. Transport: ₹3,500. Entertainment: ₹2,000. And so on until every single rupee has a destination.

Why It’s One of the Best Budgeting Methods for Complex Finances

Zero-based budgeting excels when your financial situation has multiple moving parts. Families with competing priorities — school fees, home loan EMI, vacation savings, emergency fund, retirement investment — find that broad percentage methods like 50/30/20 are too vague to actually manage these goals simultaneously.

With zero-based budgeting, each goal gets its own line, its own amount, and its own monthly tracking. You can see exactly how much progress you’re making on each front, not just a rough sense of whether you’re “doing okay.”

It’s also one of the best budgeting methods for freelancers because it starts fresh each month based on actual income — not projections. If you earned ₹38,000 last month, this month’s budget is built around ₹38,000. No assumptions, no gaps.

The Honest Challenges

Zero-based budgeting takes real time and commitment, especially in the first two or three months. You’re building the category list, estimating realistic amounts, doing weekly check-ins, and reconciling at month-end.

For someone with a very busy schedule or who finds detailed financial tracking stressful, this method can feel like a part-time job. Starting with a simpler method and graduating to zero-based when the habit is established is a completely valid approach.

Comparing All Three Methods Side by Side

When evaluating the best budgeting methods for your specific situation, a direct comparison helps cut through the noise.

| Feature | Envelope Method | Digital Budgeting | Zero-Based Budget |

|---|---|---|---|

| Setup Time | 15–20 minutes | 20–45 minutes | 45–60 minutes |

| Works With UPI/Cards | Limited | Yes | Yes |

| Best for Beginners | Yes | Yes | Takes practice |

| Handles Irregular Income | No | Somewhat | Very well |

| Tracks Specific Goals | No | Partially | Yes |

| Prevents Overspending | Very well | Moderately | Well |

| Monthly Maintenance | Low | Low–Medium | Medium–High |

No single row is all green for one method. Each has genuine trade-offs, and that’s the honest truth about the best budgeting methods conversation — there’s no universal winner.

Can You Combine These Methods?

Absolutely — and many financially organised people do exactly this without realizing it has a name.

A popular combination is using zero-based budgeting as the overall monthly plan, digital tools to track transactions automatically, and physical cash envelopes for two or three high-risk overspending categories like food and entertainment.

You get the planning precision of zero-based, the convenience of digital tracking, and the psychological friction of cash where you need it most. This hybrid approach addresses the weaknesses of each individual method while preserving their strengths.

For context on how these methods relate to broader budgeting frameworks, this comparison of the 50/30/20 rule vs. zero-based budgeting gives a useful perspective on how percentage-based and allocation-based thinking work together.

How to Pick the Right Method for Your Life Right Now

After reading about all three of the best budgeting methods, you might still be unsure which one to start with. Here’s a simple decision framework.

If you regularly overspend in one or two specific categories and need a hard stop — start with envelopes for those categories while managing the rest digitally.

If your income is stable, your expenses are predictable, and you just want an easy system to maintain awareness — digital budgeting with a good app is probably enough.

If you have significant debt, multiple savings goals, irregular income, or you’ve tried simpler methods and they haven’t been enough — zero-based budgeting is worth the extra setup time.

And if you’ve never budgeted before at all — pick whichever method on this list feels least intimidating, start imperfectly, and improve as you go. A rough budget that you actually use beats a perfect system that stays in a notebook.

What Changes in 2026 Worth Knowing

The best budgeting methods in 2026 exist in a different financial environment than even three or four years ago. A few things are worth noting.

UPI and digital payments have made cash-based systems harder to maintain for most Indian households — but they’ve also made digital tracking significantly easier with auto-SMS parsing and bank-linked apps.

Subscription costs have risen sharply. Most people now pay for multiple streaming services, cloud storage, and app subscriptions simultaneously. Any of the best budgeting methods you choose needs a dedicated subscription review built in — at minimum once every quarter.

Inflation in food and housing costs means old budget numbers go stale faster. Revisiting your category amounts every two to three months — not just annually — keeps your plan accurate and realistic.

Final Conclusion:

The search for the best budgeting methods doesn’t end with one right answer — it ends with the right answer for you. The envelope method works brilliantly for people who need physical limits to control spending. Digital budgeting fits seamlessly into a life lived on a smartphone. Zero-based budgeting gives serious financial control to anyone willing to put in the time.

What all three best budgeting methods share is this: they work when you show up for them consistently. Not perfectly. Consistently.

Pick one that fits your income type, your lifestyle, and your honest capacity for financial maintenance. Use it for three months before judging the results. Adjust what isn’t working. Add more structure as your confidence grows.

The method is just a tool. The habit of paying attention to your money — that’s what actually changes things.

Post Comment