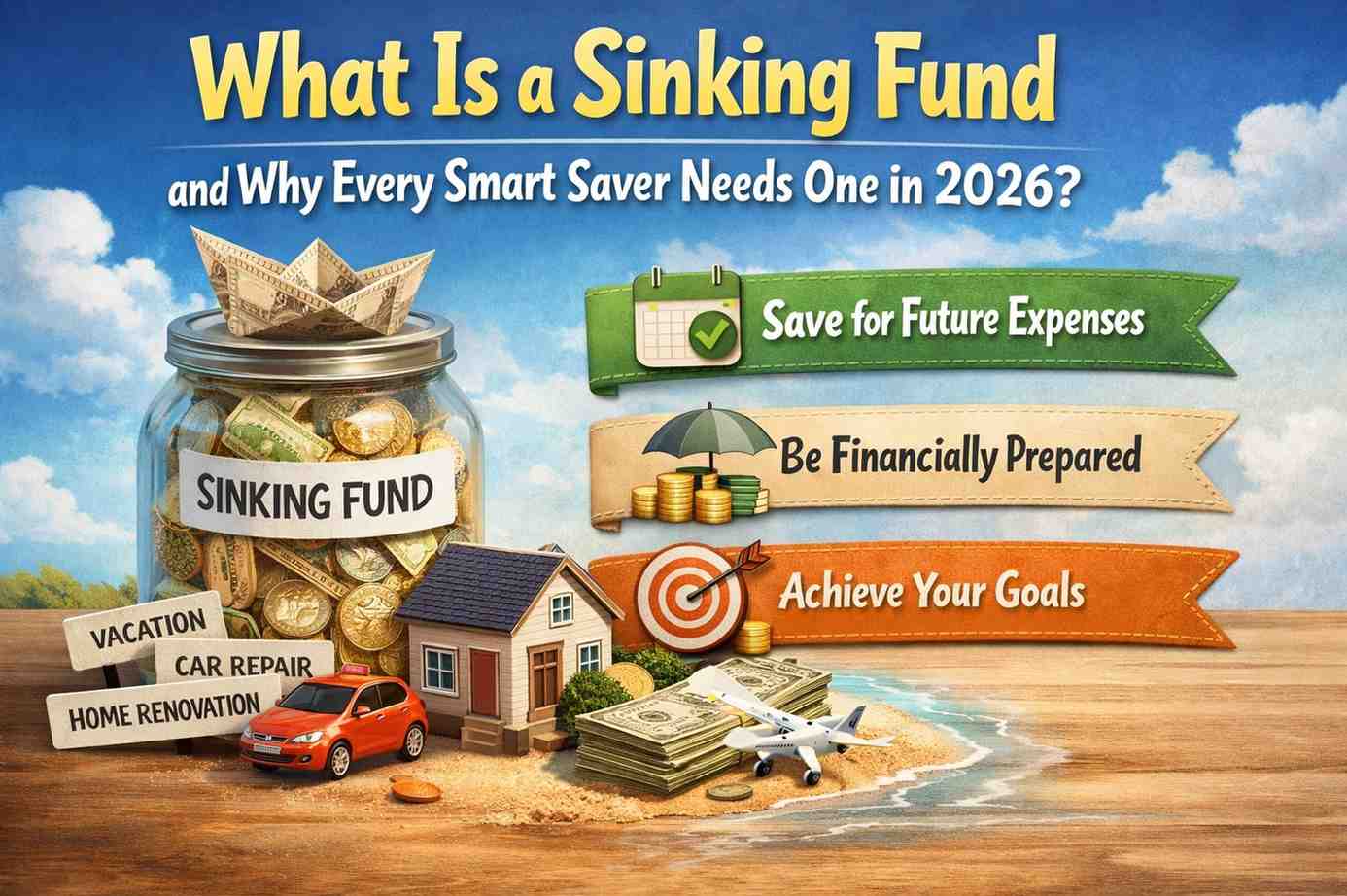

Introduction: Sinking Fund

Here’s a situation most people recognize immediately. You’ve been budgeting carefully for three months. Things are going well. Then the car needs servicing, or the annual insurance renewal arrives, or a family wedding requires new clothes and a gift — and suddenly the budget is blown, the savings account is raided, and it feels like you’re starting from zero again.

The frustrating part is that none of these expenses were actually surprises. The car always needs servicing. The insurance always renews. Weddings happen. You just didn’t plan for them in a way that protected your regular budget.

That’s exactly what a sinking fund is designed to solve. It’s one of those personal finance concepts that sounds technical until someone explains it simply — and then it becomes one of the most useful tools in your entire financial system.

This article explains what a sinking fund is, how it works in practice, why 2026 is the right time to build one into your financial life, and exactly how to set one up starting today.

The Simple Explanation of What a Sinking Fund Is

A sinking fund is money you set aside gradually, over time, for a specific future expense you know is coming.

That’s it. Nothing more complicated than that.

You identify an expense that will arrive at some predictable point — maybe in three months, maybe in eight months, maybe once a year. You calculate approximately how much it will cost. You divide that amount by the number of months until it arrives. And you set aside that monthly amount in a dedicated place, consistently, until the expense arrives.

When the bill lands, the money is already there. No panic. No budget disruption. No emergency withdrawal from savings you built for something else.

A sinking fund is the opposite of an emergency fund. An emergency fund covers genuinely unexpected, unforeseeable events — job loss, sudden illness, an accident. A sinking fund covers things that are irregular but entirely predictable — costs that happen on a cycle you already understand.

Why These Expenses Keep “Surprising” People

If annual insurance renewals and car maintenance and festival shopping happen every single year without fail, why do people keep treating them as surprises?

The honest answer is that monthly budgets naturally focus on monthly expenses. Rent is monthly. Utilities are monthly. Food is monthly. These get planned for automatically because they’re always present.

Annual and irregular expenses exist outside the monthly rhythm. They don’t show up in last month’s budget, so they don’t automatically show up in this month’s budget either. And because they’re not mentally “in” the budget, there’s no money set aside when they arrive.

A sinking fund solves this by converting irregular future expenses into small, regular monthly contributions. Instead of a ₹6,000 insurance premium arriving once a year and disrupting everything, you set aside ₹500 per month into a dedicated sinking fund for that expense. By renewal time, ₹6,000 is sitting there quietly, ready.

The Difference Between a Sinking Fund and an Emergency Fund

This confusion comes up frequently, and it’s worth clearing up properly because both funds serve different purposes and both matter.

An emergency fund is for unknown, unplanned events. You don’t know when you’ll need it, how much you’ll need, or whether you’ll need it at all this year. It exists as a financial cushion against genuine uncertainty. The standard guidance is three to six months of essential living expenses.

A sinking fund is for known, planned future costs. You know the expense is coming. You have a reasonable estimate of the cost. You’re simply spreading the financial impact across multiple months so it doesn’t hit all at once.

Using your emergency fund for predictable irregular expenses — annual fees, car servicing, appliance replacements — is one of the most common sinking fund-related mistakes people make. It depletes a safety net that exists for actual emergencies, leaving you genuinely exposed when something truly unexpected happens.

The right structure has both: an emergency fund for true unknowns, and one or more sinking funds for predictable future costs. They serve entirely different functions and shouldn’t be mixed.

What Expenses Belong in a Sinking Fund

Almost any irregular but predictable cost can and should have a dedicated sinking fund. Here’s a realistic list of the most common ones:

Annual insurance premiums — health, vehicle, life, home. These arrive on a fixed schedule with a known approximate amount.

Vehicle maintenance — servicing, tyre replacement, registration renewal. Cars need maintenance on a predictable schedule.

Medical and dental costs — routine checkups, dental cleanings, eyeglass replacements. Not emergencies — planned health maintenance.

Festival and holiday expenses — Diwali, Christmas, Eid, birthdays, family celebrations. These arrive on the exact same dates every year without exception.

Electronics replacement — your phone, laptop, or home appliances won’t last forever. Planning for replacement costs years in advance prevents them from derailing your finances.

Travel and vacation — if you take a trip annually or semi-annually, a dedicated travel sinking fund lets you pay for it comfortably without touching other savings.

Home maintenance — painting, plumbing repairs, furniture replacement, appliance servicing.

Clothing seasonal purchases — school uniforms, winter clothing, professional wardrobe updates.

Each of these becomes a separate sinking fund with its own monthly contribution amount calculated from the expected total cost divided by months remaining.

How to Calculate the Right Monthly Contribution

The math is genuinely simple. Here’s the three-step process:

Step 1 — Estimate the total cost of the expense. Be realistic, not optimistic. If your car servicing typically runs ₹4,500, use ₹5,000 to build in a small buffer.

Step 2 — Determine how many months until the expense arrives. If it’s a January expense and it’s currently July, you have six months.

Step 3 — Divide the total by the number of months. ₹5,000 divided by 6 months equals ₹834 per month.

Set aside ₹834 per month specifically for that sinking fund. By January, you have ₹5,004 ready — and your regular budget was never disrupted.

Do this calculation for every irregular expense you identify. Add all the monthly amounts together. That total is your combined sinking fund contribution — a new line in your monthly budget that transforms how predictable irregular expenses feel.

Where to Keep Your Sinking Fund Money

There are a few practical options, each with trade-offs worth understanding.

Separate Savings Account

The cleanest approach for most people is opening a dedicated savings account — separate from your main savings account — specifically for sinking fund money. This keeps the funds clearly separated from emergency savings and regular spending.

Small finance banks in India offer competitive interest rates on savings accounts with fully digital account opening on Android. Unity Small Finance Bank, Equitas, and ESAF all allow multiple account opening. The money sits safely, earns modest interest, and is easily accessible when the expense arrives.

Multiple Sub-Accounts or Virtual Envelopes

Some banks and savings apps allow you to create sub-accounts or labeled savings “pots” within one account — effectively giving each sinking fund its own labeled bucket without needing separate full accounts.

Apps like Fi Money, Jupiter, and Niyo offer this feature in India. You create a labeled goal — “Car Servicing,” “Annual Insurance,” “Diwali Fund” — and allocate money to each one separately. The visual separation helps you see exactly how much is available for each purpose without any mixing.

A Single Sinking Fund Account With a Tracking Spreadsheet

If managing multiple accounts feels like too much, keep all sinking fund money in one account and track individual fund balances in a simple Google Sheets document on your Android phone. One account, multiple virtual categories maintained in a spreadsheet — low complexity, clear visibility.

Setting Up Your First Sinking Fund Step by Step

Let’s make this concrete with a practical setup process you can start today.

Step 1 — List every irregular expense you can think of Go through the last 12 months of your bank statements. Find every non-monthly expense — anything that didn’t appear on a regular monthly schedule. Write each one down with the approximate amount.

Step 2 — Identify which ones repeat on a predictable schedule Annual insurance renewal — yes. Car met with an accident — no, that’s an emergency fund situation. Festival shopping — yes. Medical emergency — no. Sort your list into predictable versus genuinely unpredictable.

Step 3 — Calculate the monthly contribution for each For each predictable expense, divide the expected cost by the number of months until it arrives. If it’s an annual expense, divide by 12 to get the standard monthly contribution.

Step 4 — Add the total monthly contribution to your budget All your individual sinking fund contributions combined become one budget line item. For example: if your individual contributions total ₹3,200 per month across all funds, that’s ₹3,200 that moves to your sinking fund account on salary day alongside your regular savings.

Step 5 — Automate the transfer Set up a standing instruction from your salary account to your sinking fund account for the combined monthly amount. It moves automatically on salary day. You never have to decide whether to make the contribution — it happens before spending decisions begin.

For a complete framework on how sinking fund contributions fit into a structured monthly budget alongside savings and regular expenses, this guide on how to create a monthly budget plan in 5 simple steps walks through exactly how to position these contributions within your overall monthly plan.

How a Sinking Fund Changes Your Financial Stress Levels

The practical financial benefit of a sinking fund is clear — irregular expenses get covered without disrupting your budget or depleting emergency savings. But the emotional benefit is equally significant and worth acknowledging.

Financial stress frequently comes not from the expenses themselves but from the uncertainty around them. When you don’t know how you’ll handle an upcoming cost, the anxiety starts weeks or months before the expense arrives. The mental load of dreading a bill you’re not prepared for is its own form of financial burden.

A properly funded sinking fund eliminates that anticipatory stress completely. When the car service reminder arrives on your Android phone or the insurance renewal notice comes in, your reaction shifts from “how am I going to pay for this” to “good thing I’ve been saving for this.” That shift — from dread to readiness — has a real effect on day-to-day wellbeing that’s difficult to quantify but easy to feel.

Common Sinking Fund Mistakes to Avoid

Even with a clear concept and good intentions, a few predictable problems come up when people first set up a sinking fund.

Mixing sinking fund money with emergency savings — Keep them separate. Always. They serve different purposes and should live in different accounts or clearly labeled buckets.

Underestimating the expense amount — It’s better to contribute slightly more each month and have a surplus than to contribute too little and fall short. Add a 10 to 15% buffer to your estimates for categories that tend to run over.

Forgetting to start a new cycle after using the fund — When you use your annual insurance sinking fund in month 12, start contributing again from month 1 immediately. The fund needs to rebuild for next year before next year arrives.

Only creating one fund for everything — Labeling specific amounts for specific purposes is what gives the sinking fund its clarity. “Miscellaneous irregular expenses” in one unlabeled pot doesn’t create the same visibility or protection.

For context on how sinking funds fit within a broader set of budgeting habits that actually stick, this guide on how to stick to a budget every month without feeling restricted covers the behavioral side of maintaining financial systems consistently over time.

Why 2026 Makes Sinking Funds More Important Than Ever

The cost of living has increased meaningfully across most expense categories over the last few years. Insurance premiums are higher. Vehicle maintenance costs more. Seasonal expenses — festivals, travel, clothing — have all seen price increases that make irregular spending harder to absorb casually.

In this environment, the irregular expenses that were once manageable to absorb without planning have become genuinely disruptive to monthly budgets that aren’t specifically prepared for them.

A sinking fund is the most direct response to this reality. By converting irregular large costs into small regular contributions, it removes the shock of price-increased bills from your financial experience entirely. You absorb the higher cost gradually — ₹200 more per month — rather than all at once.

Additionally, with high-yield savings accounts from small finance banks offering 6 to 9% annual interest in 2026, sinking fund money can earn meaningful returns while it accumulates — particularly for funds building toward an expense that’s six to twelve months away.

Tracking Your Sinking Funds on Android

Your Android phone is sufficient to manage any number of sinking funds effectively. No specialized software required.

A simple Google Sheets document with one row per fund — fund name, target amount, monthly contribution, current balance, months remaining — gives you a complete real-time picture of all your sinking funds in one place. Update the current balance column each month when you make your contribution. When a fund is used, reset the balance to zero and update the months remaining for the next cycle.

Take two minutes on the first of each month to open the sheet, confirm the automated transfer went through, and update balances. That’s the entire maintenance requirement for a sinking fund system once it’s set up.

Set a recurring monthly reminder on your Android phone for this two-minute update. The reminder is the only thing standing between “set up and forgot” and “actively maintained and working.”

Final Conclusion: Sinking Fund

A sinking fund is one of those financial tools that seems almost too simple to be as effective as it is. Set aside money regularly for something you know is coming. That’s the whole concept.

But the effect of applying that simple concept consistently across all your irregular predictable expenses is genuinely transformative. Budgets stop getting disrupted by expenses that were never really surprises. Emergency savings stop getting raided for costs that were always predictable. Financial stress around upcoming bills drops significantly because readiness replaces dread.

Start with your single largest irregular annual expense — probably insurance, a vehicle cost, or a major seasonal spending event. Calculate the monthly contribution. Open a separate account or create a labeled digital pot. Set up the automated transfer. Run it for three months and observe what it feels like to know that money is building toward a specific purpose.

Then add the next sinking fund. And the next. Over six months, you’ll have a complete system that makes the financial calendar feel manageable rather than threatening — month by month, expense by expense, contribution by contribution.