Introduction: Cash Stuffing vs. Digital Savings

If you’ve spent any time on personal finance content recently — YouTube, Instagram, financial blogs — you’ve probably seen both of these methods come up. Cash stuffing has become genuinely popular over the last few years, with people showing colorful envelopes and binders full of sorted cash. Digital savings, on the other hand, is what most people default to without ever consciously choosing it.

The cash stuffing vs. digital savings conversation is more interesting than it first appears. Because this isn’t just a question of which one technically produces more interest. It’s a question of which method actually changes spending behavior, builds saving habits, and produces real financial results for real people over time.

This guide breaks down both methods honestly — how each works, what each costs, where each fails, and which one genuinely grows your money faster depending on how your brain and spending habits actually work.

What Cash Stuffing Actually Is and How It Works

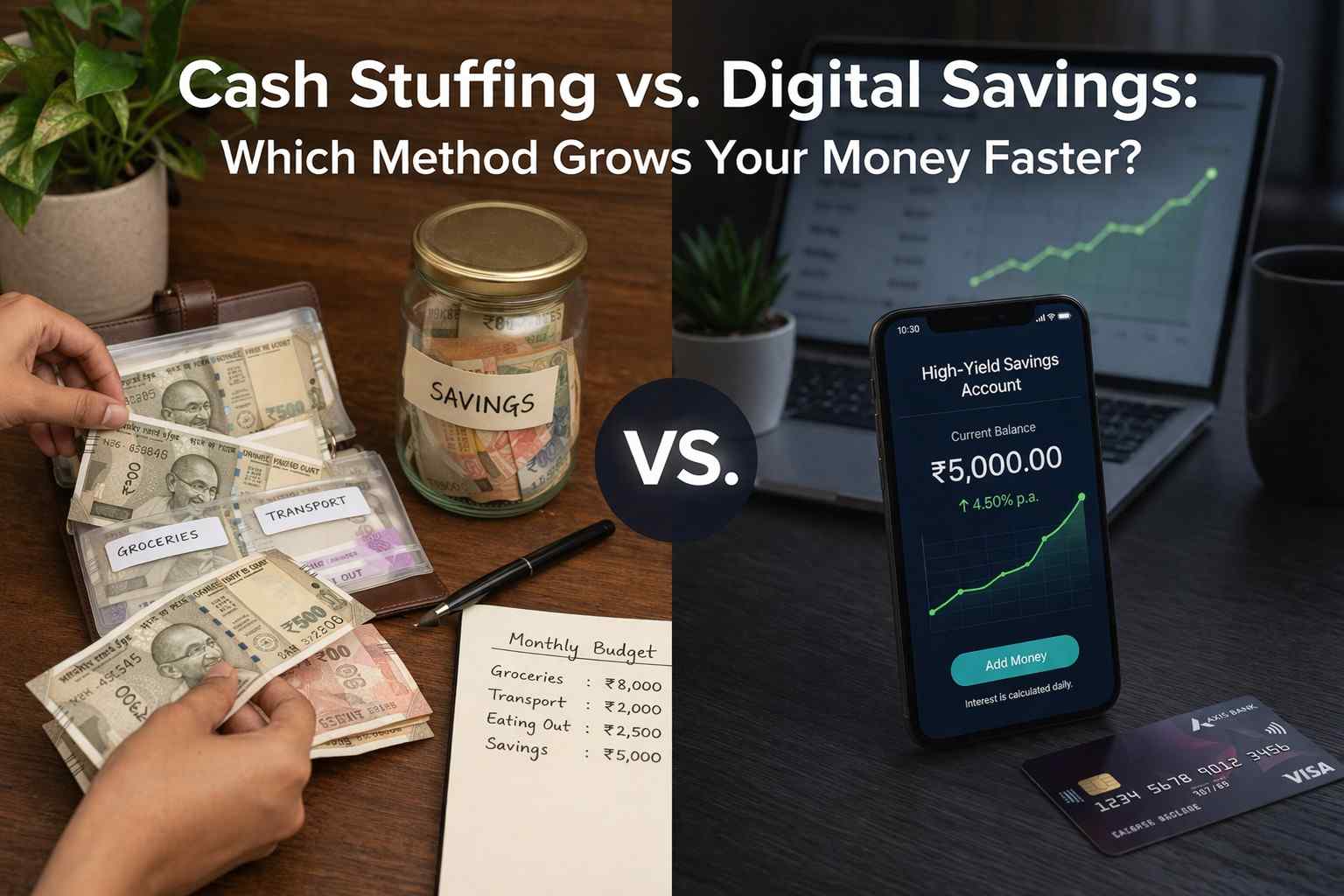

Cash stuffing is a physical budgeting method based on the original envelope system. You withdraw your entire monthly budget in cash at the start of the month, divide it into labeled envelopes or a dedicated binder with category pouches, and spend only from the relevant envelope for each type of purchase.

Groceries envelope. Transport envelope. Entertainment envelope. Personal care envelope. When a particular envelope runs out, spending in that category stops — full stop. No borrowing from next month. No transferring from another envelope without a conscious, deliberate decision.

The “stuffing” part refers to the act of physically placing cash into each envelope or pouch at the start of the month. For many people, this physical ritual creates a connection to their budget that looking at numbers on a screen simply doesn’t replicate.

In the cash stuffing vs. digital savings comparison, cash stuffing is fundamentally a spending control tool first and a savings method second. The savings come from what’s left in envelopes at month end — and from the reduced spending that physical cash limits naturally produce.

What Digital Savings Actually Is

Digital savings covers a broad range of approaches — from simply leaving money in a standard savings account, to using dedicated savings apps, to setting up automated transfers to high-yield accounts on salary day.

The common thread is that everything happens electronically. No physical cash changes hands. Spending happens via UPI, debit card, or credit card. Savings transfers happen automatically or manually through mobile banking apps on your Android phone.

Digital savings is what most people in urban India already do by default — even if they’ve never consciously set it up as a system. Your salary lands in your account, some bills get paid automatically, and whatever remains at the end of the month is loosely considered “savings.”

The problem with that passive version of digital savings is that it produces inconsistent, often disappointing results. The more intentional version — automated transfers, dedicated savings accounts, high-yield options — is a genuinely different proposition and the one worth comparing seriously against cash stuffing.

The Psychological Difference Between the Two Methods

This is where the cash stuffing vs. digital savings comparison gets genuinely interesting — and where the answer for most people becomes clear.

Physical cash activates different psychological responses than digital money. Multiple studies in behavioral economics have documented what most people intuitively know: spending cash hurts more than spending digitally. Handing over physical notes creates a visceral awareness of money leaving that tapping a phone or swiping a card simply doesn’t trigger.

This phenomenon — sometimes called the “pain of paying” — is why people who pay with cash consistently spend less than people who pay with cards for identical purchases. The friction isn’t inconvenience. It’s psychological awareness.

Cash stuffing deliberately weaponizes this psychology. When you open your grocery envelope and physically count out the remaining cash before a shopping trip, you know exactly where you stand. No app required. No checking balance. The information is in your hands, literally.

Digital payments remove this friction almost entirely — which is convenient and also expensive if you’re someone whose spending responds to friction. In the cash stuffing vs. digital savings debate, this psychological dimension matters more than most financial comparisons acknowledge.

Where Cash Stuffing Falls Short

The psychological advantages of cash stuffing are real. The practical limitations in 2026 are also real — and they matter significantly for most Indian urban consumers.

Most Transactions Are Digital Now

Rent, utility bills, insurance premiums, online shopping, food delivery, streaming subscriptions, mobile recharge — the majority of regular monthly expenses for most urban Indians cannot be paid in cash even if you want to. These transactions happen electronically by nature.

This means a pure cash stuffing system simply can’t cover your entire budget. You’d need to maintain separate digital accounts for fixed and online expenses while using cash envelopes only for in-person variable spending — which adds complexity rather than reducing it.

Cash Earns Zero Interest

This is the most concrete financial disadvantage in the cash stuffing vs. digital savings comparison. Physical cash in an envelope earns absolutely nothing. Zero percent return. Every month that ₹8,000 sits in envelopes is a month it could have been earning 6–8% annually in a high-yield savings account.

On ₹10,000 held throughout a month, the interest opportunity cost is small individually. But multiplied across 12 months, and across several categories of cash held simultaneously, the foregone interest adds up to a real amount — particularly if you maintain a substantial cash float.

Security and Practicality

Physical cash can be lost, stolen, or damaged. It can’t be recovered the way digital transactions can. It requires a visit to an ATM before the month starts — a logistical step that adds friction to the process.

For families with multiple spending members, distributing cash requires physical handoff. Digital transfers happen in seconds from anywhere.

Where Digital Savings Falls Short

Digital savings has equally real limitations — particularly for people whose spending behavior doesn’t respond well to invisible money.

The “Out of Sight, Spends Easily” Problem

When all your money lives in digital accounts and all transactions happen with taps and swipes, most people genuinely lose track of where they stand within a month. The spending doesn’t feel real in the same way physical cash does.

This is why so many people who earnestly try to budget digitally still find themselves surprised at month end by how much they spent. The transactions happened too easily, too frictionlessly, and too invisibly for behavioral awareness to catch up with the actual spending.

Automation Without Awareness Isn’t Enough

A lot of digital savings advice focuses on automation — set up auto-transfers, use spending tracking apps, let the system handle it. Automation is genuinely useful. But automation without active engagement produces people who have technically saved money but have no real awareness of their spending patterns or financial situation.

In the cash stuffing vs. digital savings comparison, digital savings done passively — just letting money sit in an account without any intentional system — consistently underperforms what people expect from it.

App Fatigue and Notification Blindness

Budgeting apps require consistent engagement to produce results. Many people download them, use them enthusiastically for two weeks, and gradually stop checking them. The notifications become background noise. The data accumulates but no one looks at it.

Which Method Actually Grows Money Faster — The Honest Answer

The direct answer to the cash stuffing vs. digital savings question depends entirely on which limitation causes more damage for you personally.

If your primary financial problem is overspending — you earn a decent income but consistently have nothing left at month end because money slips through unnoticed — cash stuffing will grow your savings faster. The behavioral friction it creates reduces spending more effectively than any digital tool for people whose spending responds to physical awareness. More spending control means more money available to save, which outweighs the interest rate disadvantage.

If your primary financial problem is not saving consistently — you spend reasonably well but fail to put money away because it never feels like the right time — automated digital savings will grow your money faster. Automation removes the decision point entirely, and the higher interest rates on dedicated savings accounts compound the advantage over time.

For most people, the honest answer involves elements of both — which leads to the most practical conclusion in the entire cash stuffing vs. digital savings discussion.

The Hybrid Approach — Using Both Methods Together

Many financially organized people in 2026 use a version of both systems simultaneously, each serving a different function.

Digital automation handles the savings side. Salary arrives, an automatic transfer moves a fixed savings amount to a high-yield savings account immediately — before any spending happens. Emergency fund, investment contributions, and goal-based savings all happen digitally and automatically. This captures the interest rate advantage and removes saving from the realm of willpower.

Physical cash or a cash-stuffing-inspired digital envelope system handles the variable spending side. For categories where overspending is a personal pattern — usually food, entertainment, and personal care — having a visible, finite limit creates the behavioral friction that reduces waste spending.

On Android, apps like Goodbudget replicate the envelope system digitally — each category gets a virtual envelope with a set amount, and you log transactions against the relevant envelope. This captures some of the awareness benefit of cash stuffing without requiring physical currency. It’s not identical to the psychological impact of real cash, but it’s significantly more practical for a primarily digital spending life.

The cash stuffing vs. digital savings hybrid means you’re not choosing between behavioral control and financial returns. You’re getting both — from a combined system that uses each method where it works best.

How to Set Up the Hybrid System on Your Android Phone

Setting up a practical hybrid system takes less than a weekend afternoon and requires no expensive tools.

Step 1 — Automate Your Savings First

Open a separate high-yield savings account — Unity Small Finance Bank, ESAF, or IDFC FIRST Bank all offer competitive rates with fully digital account opening via Android. Set up a standing instruction to transfer your monthly savings amount on the day after salary credit. This happens automatically, before any spending decisions occur.

Step 2 — Identify Your Two or Three Overspending Categories

Look at your last two months of transaction history. Find the categories where actual spending consistently exceeds what you’d comfortably call intentional. These are your cash-stuffing candidates — the categories where physical or envelope-style limits will produce the most behavioral benefit.

Step 3 — Apply Cash or Digital Envelopes to Those Categories

Either withdraw cash specifically for those categories at the start of the month, or use a free envelope budgeting app on your Android phone to create virtual envelopes with hard limits. Update these envelopes every time you spend from those categories.

For a complete framework on how these categories fit into a structured monthly budget, this guide on creating a monthly budget plan in 5 simple steps shows exactly how to build the overall structure that supports both automated savings and envelope-style spending control.

Step 4 — Review Weekly, Not Monthly

Both cash stuffing and digital savings work better with regular engagement than with monthly-only check-ins. Set a weekly Sunday reminder on your phone — ten minutes to check your envelope balances, confirm your savings transfer went through, and note any adjustments needed for the following week.

The Interest Rate Reality for Long-Term Savings

For anyone holding savings for more than a few months, the interest rate difference between cash stuffing and digital savings becomes financially significant in a way that deserves direct attention.

Cash: 0% return. Always.

Standard savings account: approximately 2.7–3% annually.

High-yield savings account (small finance banks in 2026): approximately 6–9% annually depending on balance tier and institution.

On ₹50,000 held for one year, the difference between 0% and 7% is ₹3,500. On ₹2,00,000, it’s ₹14,000 — earned passively, with zero additional effort after the account is opened.

This reality means that while cash stuffing is a powerful spending control tool, it should never be used as a long-term storage method for money you’re genuinely accumulating. Any savings that won’t be spent within the current month should live in a digital account where it earns a real return.

For context on which savings accounts offer the best rates for everyday savers in 2026, this comparison of the best high-yield savings accounts covers the most relevant options with honest rate comparisons.

Who Should Use Which Method — A Quick Decision Guide

After working through the full cash stuffing vs. digital savings comparison, here’s a practical decision framework based on your specific financial situation.

Use cash stuffing as your primary variable spending tool if — you consistently overspend in specific categories despite knowing your budget, you feel disconnected from your spending because everything happens digitally, or you’ve tried tracking apps multiple times and stopped using them within a month.

Use digital savings as your primary savings method if — you’re building an emergency fund, saving toward a specific goal, or accumulating money over multiple months. Always. The interest rate advantage is too significant to leave on the table for any amount held beyond the current month.

Use the hybrid approach if — your financial situation has both a spending control problem and a savings consistency problem, which describes the majority of people honestly examining their monthly finances.

Final Conclusion: Cash Stuffing vs. Digital Savings

The cash stuffing vs. digital savings debate doesn’t have a single winner that works for everyone in every situation. What it has is a clear understanding of what each method does well and where each one falls apart.

Cash stuffing wins on behavioral psychology — it makes spending feel real, creates natural limits, and reduces unconscious overspending for people whose habits respond to physical friction. Digital savings wins on financial returns, automation, and practicality in a world where most transactions happen electronically.

The most honest answer to which method grows your money faster is this: digital savings grows accumulated money faster through interest rates and automation. Cash stuffing grows available money to save by reducing the spending that currently prevents saving in the first place.

Use both where each works best. Automate your savings digitally into accounts that pay real interest. Apply physical or envelope-style limits to the spending categories where awareness and friction produce the most behavioral change.

That combination — not a choice between the two — is what consistently produces the best financial outcomes for real people managing real monthly budgets in 2026.