50/30/20 Rule vs. Zero-Based Budget: Which Method Works Best for You?

Introduction: 50/30/20 Rule vs. Zero-Based Budget

Choosing a budgeting method feels simple until you actually sit down and try to pick one. There’s no shortage of advice online — but most of it either oversimplifies things or makes both methods sound equally great without giving you any real way to decide.

The 50/30/20 rule vs. zero-based budget debate has been going on in personal finance circles for years. And honestly, both sides have a point. These two methods work — just not for the same people, in the same situations, at the same time.

This article breaks down both approaches in plain language, compares them honestly, and helps you figure out which one actually fits your life right now.

What the 50/30/20 Rule Actually Means

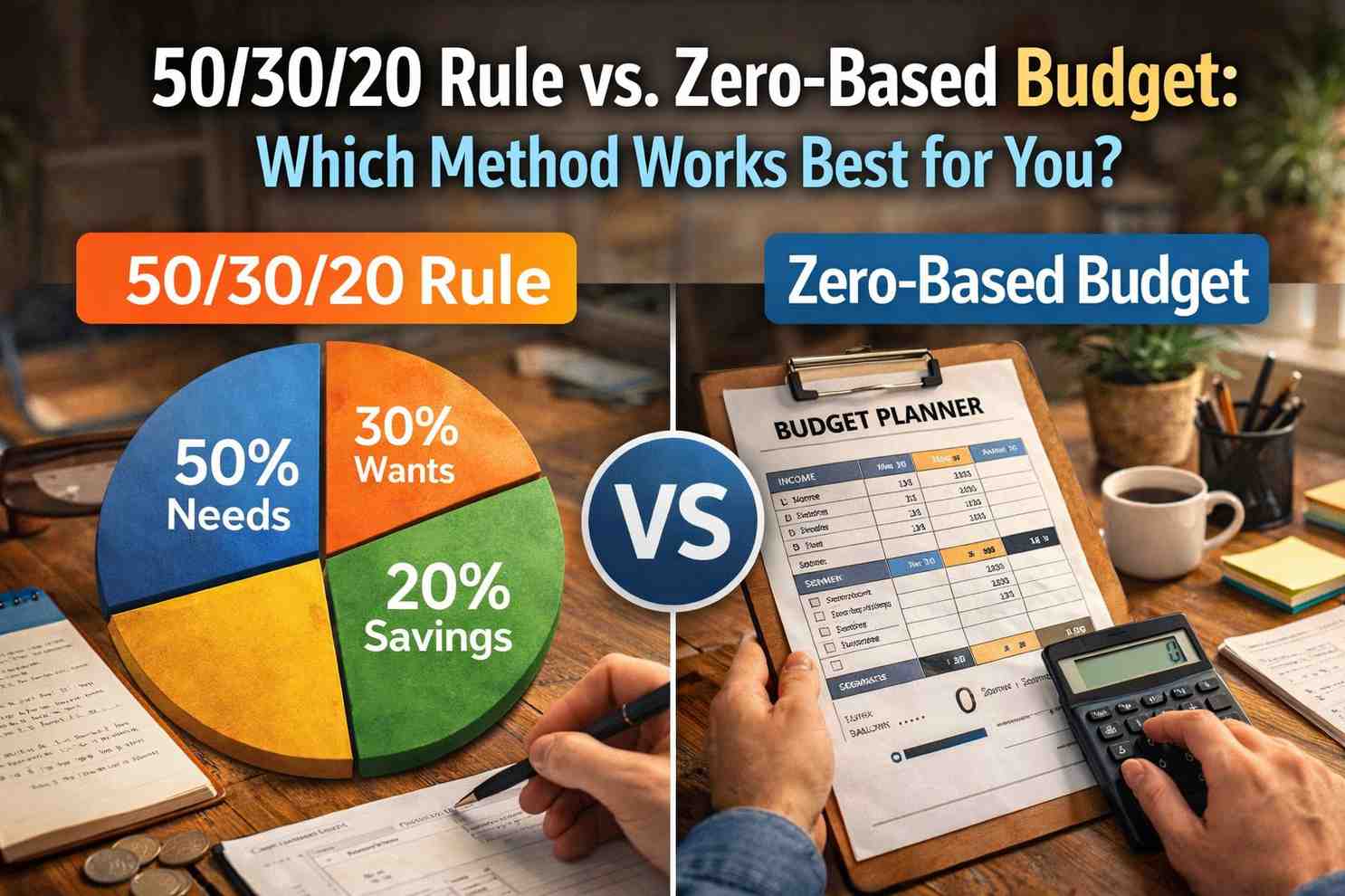

The 50/30/20 rule is a percentage-based budgeting method. It divides your take-home income into three broad buckets.

50% goes toward needs — rent, food, utility bills, transport. 30% goes toward wants — dining out, entertainment, shopping, subscriptions. The remaining 20% goes toward savings and debt repayment.

That’s the whole framework. If you take home ₹50,000 a month, roughly ₹25,000 covers needs, ₹15,000 covers wants, and ₹10,000 goes to savings. Simple math, clear categories.

The appeal is obvious. You don’t need a spreadsheet, you don’t need to track every transaction, and you can set it up in about ten minutes.

What Zero-Based Budgeting Actually Means

Zero-based budgeting works differently. Instead of splitting income by percentages, you assign every single rupee a specific purpose — until your income minus your expenses equals exactly zero.

You’re not spending everything. You’re allocating everything. Savings gets a job. Investments get a job. Even that ₹1,000 “just in case” buffer gets a category and a number attached to it.

It’s more detailed than the 50/30/20 rule vs. zero-based budget comparison might suggest at first glance. Yes, it takes more time to set up. But for that extra effort, you get something the percentage method simply can’t give you — granular, honest control over where your money actually goes.

If you’re completely new to this approach, this step-by-step guide on how to build a zero-based budget from scratch walks you through the full process with a free template.

The Core Philosophical Difference

When comparing the 50/30/20 rule vs. zero-based budget, the most important thing to understand isn’t the mechanics — it’s the mindset behind each method.

The 50/30/20 rule is built on simplicity and flexibility. It gives you guardrails, not rigid rules. As long as your spending stays roughly within those three percentage bands, you’re doing fine.

Zero-based budgeting is built on intentionality and precision. Every spending decision is made in advance. Nothing floats around without a destination. There’s no “I’ll figure it out later” category.

Neither is better in an absolute sense. They just solve different problems for different types of people.

Who the 50/30/20 Rule Works Best For

Not everyone needs a detailed, category-by-category budget. For some people, the 50/30/20 rule is genuinely the right tool.

Salaried Employees With Predictable Income

If your salary hits your account on the same date every month and your expenses don’t change much, the 50/30/20 split gives you enough structure without demanding constant attention. A quick check at month-end to confirm your buckets look right — and you’re done.

Complete Beginners to Budgeting

If you’ve never budgeted before, jumping straight into zero-based budgeting can feel overwhelming. There are categories to create, amounts to assign, and weekly check-ins to maintain. The 50/30/20 rule is a softer entry point.

It builds the habit of paying attention to money without requiring perfection. Many financial coaches actually recommend starting here for the first few months before moving to something more structured.

People With Simple Financial Lives

Someone early in their career, renting a small flat, with no dependents and minimal debt — the 50/30/20 rule is probably enough. There aren’t many variables to manage, so a broad framework handles things well.

Who Zero-Based Budgeting Works Best For

The 50/30/20 rule vs. zero-based budget comparison shifts significantly when life gets more complicated.

Freelancers and Self-Employed People

Freelancers often have irregular income — some months are excellent, some are slow. Percentage-based budgeting becomes awkward when the base number changes every single month. Zero-based budgeting, on the other hand, starts with whatever you actually earned last month and builds the plan from there.

This removes the anxiety of projecting future income and creates real structure even when cash flow is unpredictable.

People Aggressively Paying Off Debt

If your goal is to eliminate a loan or credit card balance as fast as possible, you need to know exactly how much is being directed toward that goal each month. A vague “20% toward savings and debt” category doesn’t give you that precision.

Zero-based budgeting lets you carve out a specific debt repayment line item, track it separately from savings, and see real progress every month.

Families Managing Multiple Financial Goals

A family handling school fees, a home loan EMI, an emergency fund, a vacation savings goal, and monthly grocery costs for four people — the 50/30/20 rule starts to feel too broad. There are too many competing priorities sitting inside those three buckets.

Zero-based budgeting handles this well because every goal gets its own category and its own monthly number.

A Side-by-Side Honest Comparison

Let’s look at the 50/30/20 rule vs. zero-based budget directly, without sugarcoating either one.

| Feature | 50/30/20 Rule | Zero-Based Budget |

|---|---|---|

| Setup Time | 10–15 minutes | 45–60 minutes |

| Flexibility | High | Moderate |

| Best for irregular income | No | Yes |

| Tracks exact spending | No | Yes |

| Good for beginners | Yes | Takes practice |

| Works for complex goals | Limited | Very well |

| Monthly maintenance | Low | Medium–High |

Neither column is all green or all red. That’s the honest answer. Your life circumstances determine which column matters more right now.

The Biggest Weakness of Each Method

No budgeting system is perfect. Both the 50/30/20 rule vs. zero-based budget methods have real limitations worth knowing before you commit.

Where the 50/30/20 Rule Falls Short

The biggest problem is that 50% for “needs” doesn’t work in high cost-of-living cities. If you live in Mumbai or Bangalore, rent alone might eat 40–45% of your take-home salary. Add food, transport, and utilities — you’re already past 50% before you’ve bought a single “want.”

The framework also doesn’t distinguish between different kinds of savings goals. Putting ₹5,000 into an emergency fund feels very different from putting ₹5,000 into a retirement account — but the 50/30/20 rule treats both the same.

Where Zero-Based Budgeting Falls Short

It’s time-consuming, especially in the first two or three months. You have to build the category list, estimate amounts, track spending weekly, and reconcile at month-end. For someone with a busy schedule or multiple dependents, this can genuinely feel like a part-time job.

It can also become rigid if you’re not careful. Life doesn’t always fit into pre-assigned categories. An unexpected expense can throw off the whole plan if you haven’t built in a buffer or a miscellaneous category.

Can You Combine Both Methods?

Actually, yes — and a lot of people do this without realizing it has a name.

You can use the 50/30/20 rule as your starting point to set broad category limits, then apply zero-based thinking within those categories. For example: you decide 20% of your income goes to financial goals (50/30/20 logic), then you break that 20% down specifically — ₹3,000 emergency fund, ₹4,000 mutual fund SIP, ₹2,000 vacation savings (zero-based logic).

This hybrid approach gives you the simplicity of percentage thinking at the top level and the precision of zero-based thinking where it actually matters most — your savings and debt categories.

For a deeper look at how this combination works in practice, this guide on personal budgeting strategies for variable incomes covers real examples worth reading.

How to Actually Choose Between the Two

If you’re still unsure after reading all of this, ask yourself these three questions honestly.

First — How stable is your income? If it changes month to month, zero-based budgeting fits better. If it’s consistent, either method works.

Second — How specific are your financial goals right now? If you have one or two simple goals like “save more” and “pay off a small debt,” the 50/30/20 rule is enough. If you have five or six goals competing for the same money, you need zero-based structure.

Third — How much time can you realistically give to this? Be honest. A zero-based budget you abandon after two weeks is worse than a 50/30/20 plan you stick with for six months. The best 50/30/20 rule vs. zero-based budget answer is whichever one you’ll actually maintain.

Making the Switch From One Method to the Other

Some people start with 50/30/20 and outgrow it. That’s completely normal. As your income grows, your expenses become more complex, or your goals become more specific — the percentage-based approach starts to feel a bit too loose.

When that happens, switching to zero-based budgeting isn’t starting over. All those months of tracking your spending with the 50/30/20 rule have given you real data — you already know roughly what you spend on food, transport, and entertainment. Zero-based budgeting just takes that data and makes it more precise.

The transition usually takes one or two months to feel natural. Give yourself that adjustment period without judging the results too harshly.

A Quick Note on Budgeting Apps in 2026

Whether you go with the 50/30/20 rule vs. zero-based budget, the right app can make either method significantly easier to maintain.

For 50/30/20 users, apps like Walnut or Money Manager work well — they auto-categorize spending and show you which bucket you’re in at a glance. For zero-based budgeting, YNAB (You Need A Budget) is the most dedicated tool available, though it comes with a subscription cost. A free Google Sheets template works just as well if you prefer something manual and customizable.

The app is just a tool, though. The thinking has to happen in your head first.

Final Conclusion: 50/30/20 Rule vs. Zero-Based Budget

The 50/30/20 rule vs. zero-based budget isn’t really a competition — it’s a spectrum. One end offers simplicity and ease of use. The other offers control and precision. Where you should sit on that spectrum depends entirely on your income type, your financial goals, and how much time you’re genuinely willing to put in.

If you’re just starting out, the 50/30/20 rule builds the habit without the overwhelm. If you’re ready for something more serious — dealing with debt, irregular income, or multiple competing goals — zero-based budgeting gives you the clarity that percentages alone can’t offer.

Start somewhere. Stay consistent. Adjust as your life changes. That’s the actual secret to making either method work.

Post Comment